Property owners in Las Vegas face a common misconception about insurance coverage. Many assume their standard homeowners policy will protect rental properties.

We at Invest America Insurance see this mistake regularly. The landlord insurance vs homeowners insurance debate affects thousands of Nevada investors who risk significant financial exposure without proper coverage.

How Does Landlord Insurance Actually Work

Landlord insurance protects business assets rather than personal residences, which creates fundamental differences from homeowners coverage. The National Association of Insurance Commissioners shows that homeowners insurance premiums rose by 11.2 percent in 2022, reflecting increased costs across property insurance markets including landlord policies.

Property damage coverage extends beyond basic perils to include tenant-caused damage, vandalism, and malicious destruction that homeowners policies typically exclude. Liability protection reaches higher limits because landlords face exposure from tenant injuries, guest accidents, and property-related lawsuits that can exceed $1 million in Las Vegas’s litigation-heavy environment.

Loss of Rental Income Protection Changes Everything

The most significant difference lies in rental income coverage, which homeowners insurance never provides. This protection pays landlords when properties become uninhabitable due to covered damages and maintains cash flow during repairs.

Las Vegas landlords receive 80% to 100% of monthly rent for up to 12 months (depending on policy terms) when they use this coverage. Tenant screening quality directly affects premium costs, with professional background checks reducing rates by 10% to 15% according to industry data.

The number 100% seems to be not appropriate for this chart. Please use a different chart type.

Location Impact on Premium Costs

Property location matters extensively in Nevada, where crime rates in certain Las Vegas neighborhoods can double insurance costs compared to Henderson or Summerlin properties. Insurance companies analyze neighborhood statistics, proximity to fire stations, and local crime data when they calculate premiums.

Properties in high-crime areas face surcharges that can add $500 to $1,200 annually to standard rates. Commercial districts and areas with frequent police calls trigger automatic premium increases across most carriers.

Coverage Exclusions Hit Landlords Harder

Landlord policies exclude normal wear and tear, intentional tenant damage, and flood damage more strictly than homeowners insurance. Nevada landlords must purchase separate flood coverage even for properties outside FEMA flood zones because flash floods affect rental properties disproportionately.

Vacant property periods exceeding 30 days trigger coverage restrictions or complete exclusions, which makes tenant turnover management financially critical. These exclusions directly impact how landlords structure their coverage needs and budget for comprehensive protection.

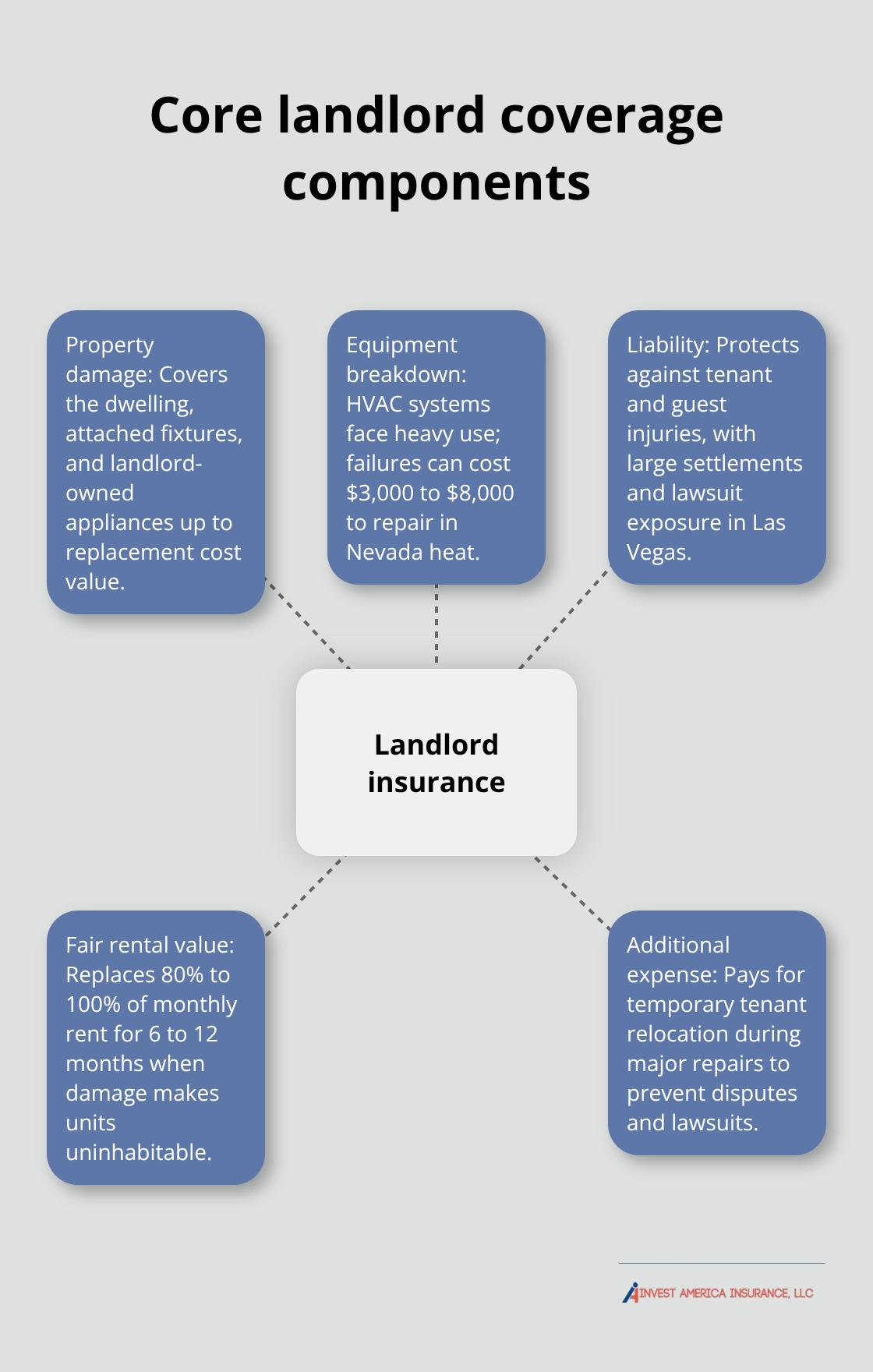

Key Coverage Areas in Landlord Insurance

Property Damage Protection Beyond Standard Homeowners Policies

Landlord insurance covers dwelling protection that extends far beyond what homeowners policies offer. Rental properties face increased property damage risks from water damage due to delayed maintenance, fire from resident negligence, and vandalism during vacancies. Nevada landlords need coverage for malicious tenant damage, which can include punched walls, broken fixtures, carpet destruction, and appliance abuse that homeowners insurance completely excludes.

Standard policies protect the building structure, attached fixtures, and landlord-owned appliances up to replacement cost value. Las Vegas properties require specialized coverage for HVAC systems, which face accelerated wear from constant use and poor tenant maintenance. Smart landlords purchase additional equipment breakdown coverage because air conditioning failures cost $3,000 to $8,000 to repair in Nevada’s extreme heat.

Liability Coverage Handles Tenant and Guest Injuries

Tenant injury claims hit landlords with average settlements of $85,000 according to recent industry data, which makes liability protection the most financially significant coverage area. Nevada landlords face exposure when tenants slip on icy walkways, trip over broken stairs, suffer electrical shocks from faulty wires, or experience carbon monoxide exposure from defective heat systems.

Guest injury claims create even higher liability exposure because visitors lack familiarity with property hazards. Pool accidents, balcony collapses, and security-related assaults generate million-dollar lawsuits that standard homeowners liability limits cannot handle. Professional landlords carry $1 million to $2 million in liability coverage because Las Vegas juries award substantial damages in premises liability cases.

Fair Rental Value Protection Maintains Cash Flow

Fair rental value coverage replaces lost income when covered damage makes properties uninhabitable (which homeowners insurance never provides). This protection pays 80% to 100% of monthly rent for 6 to 12 months based on policy terms and repair complexity. Las Vegas landlords collect an average of $1,800 monthly rent according to recent market data, which makes rental income loss coverage worth $10,800 to $21,600 during extended repairs.

Additional expense coverage pays for temporary tenant relocation when landlords must move tenants during major repairs. This coverage prevents expensive lawsuits and maintains positive tenant relationships that protect long-term rental income. These cost factors and premium considerations directly affect how much landlords pay for comprehensive coverage.

Cost Factors and Premium Considerations

Location Impact on Insurance Rates

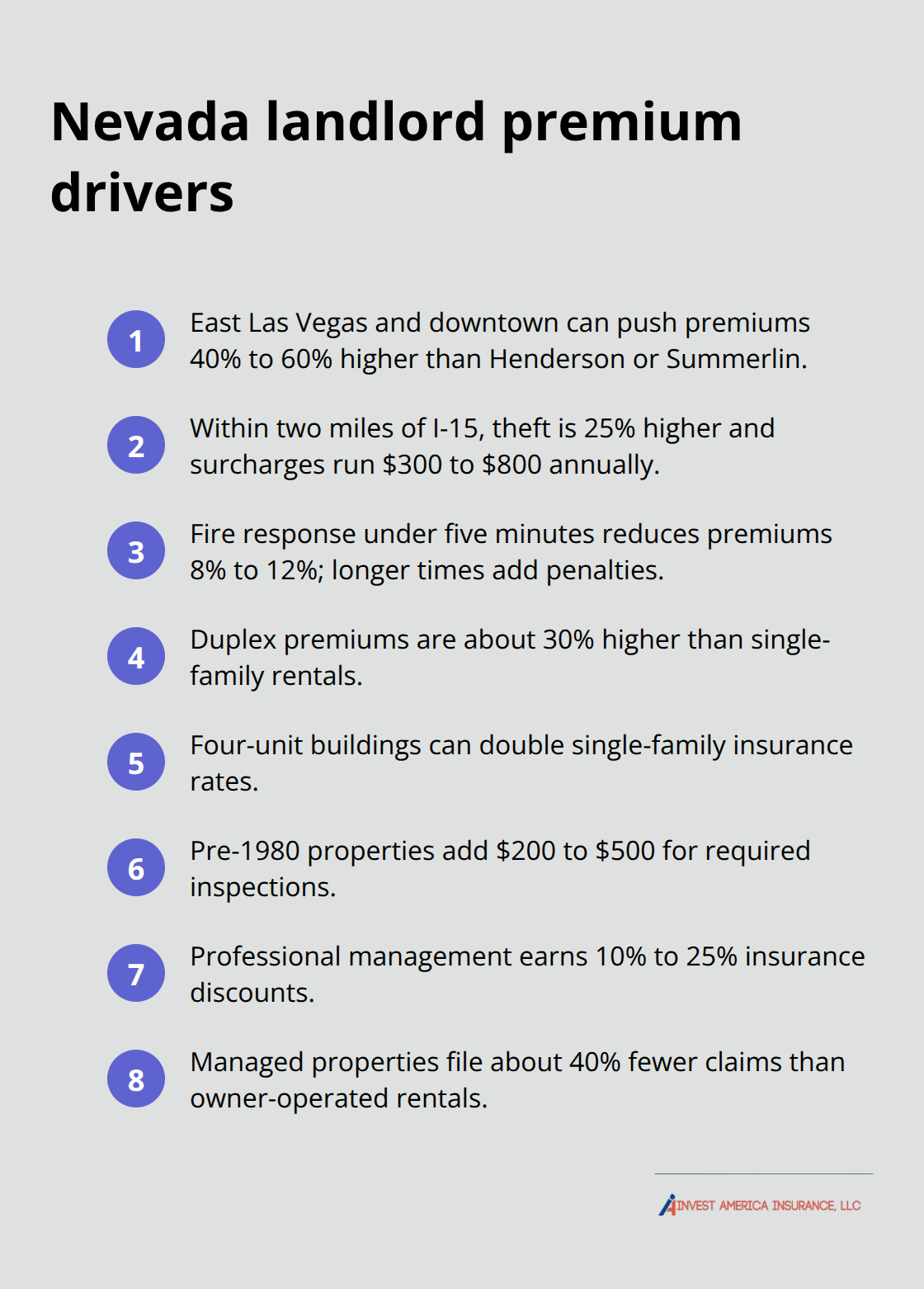

Property location dominates premium calculations more than any other factor in Nevada’s insurance market. Las Vegas neighborhoods like East Las Vegas and downtown areas face crime rates that push annual premiums 40% to 60% higher than Henderson or Summerlin properties according to Nevada Department of Insurance data. Insurance companies track ZIP code statistics for burglary, vandalism, and assault incidents when they calculate base rates.

Properties within two miles of Interstate 15 corridors experience 25% higher theft rates, which automatically triggers premium surcharges of $300 to $800 annually. Fire station proximity affects costs significantly because response times under five minutes reduce premiums by 8% to 12%, while properties beyond ten minutes face penalty surcharges.

Property Type and Unit Count Effects

Multi-unit properties create exponential cost increases rather than linear structures. Duplex properties cost 30% more than single-family rentals, while four-unit buildings face premiums that double single-family rates. Property age matters extensively because buildings constructed before 1980 require electrical and plumbing inspections that add $200 to $500 to annual costs.

Older properties contain hazardous materials like lead or asbestos that increase liability exposure and premium costs. Insurance carriers assess these risks through mandatory inspections before they issue coverage for pre-1980 buildings.

Tenant Management and Risk Reduction

Tenant screening quality directly impacts premium calculations, with professional background checks and income verification available through Nevada tenant screening services. Properties managed by professional companies receive discounts of 10% to 25% because managed properties file 40% fewer claims than owner-operated rentals (according to Insurance Information Institute research).

Las Vegas landlords who implement security systems, conduct quarterly inspections, and maintain detailed tenant documentation consistently secure the lowest available rates across all major carriers. These risk management practices demonstrate to insurers that landlords take proactive steps to prevent claims and protect their investments.

Final Thoughts

The landlord insurance vs homeowners insurance distinction affects every Las Vegas property investor’s financial security. Homeowners insurance protects personal residences and belongings, while landlord insurance covers rental properties with specialized protections for tenant-related risks, property damage, and lost rental income. Las Vegas landlords face unique exposures that homeowners policies never address.

Tenant injuries, malicious damage, and rental income loss create financial risks that can exceed $100,000 per incident. Standard homeowners coverage excludes these rental-specific perils entirely. Property location, tenant quality, and risk management practices directly impact premium costs in Nevada’s competitive insurance market (with professional tenant screening and property management reducing claims frequency and securing better rates across all carriers).

We at Invest America Insurance work with multiple carriers to find competitive landlord insurance options for Las Vegas property investors. As an independent agency, we shop coverage options and provide clear explanations of policy terms to help you protect your rental property investments. Contact us today for personalized landlord insurance quotes that match your specific property risks and coverage needs.