Buying your first home is one of the biggest financial decisions you’ll make. Home insurance for first-time buyers isn’t optional-it’s a requirement from your lender and your best protection against unexpected losses.

We at Invest America Insurance know that navigating coverage options, deductibles, and premiums can feel overwhelming. This guide breaks down everything you need to know to find the right policy for your Las Vegas home.

What Your Home Insurance Actually Covers and Why the Details Matter

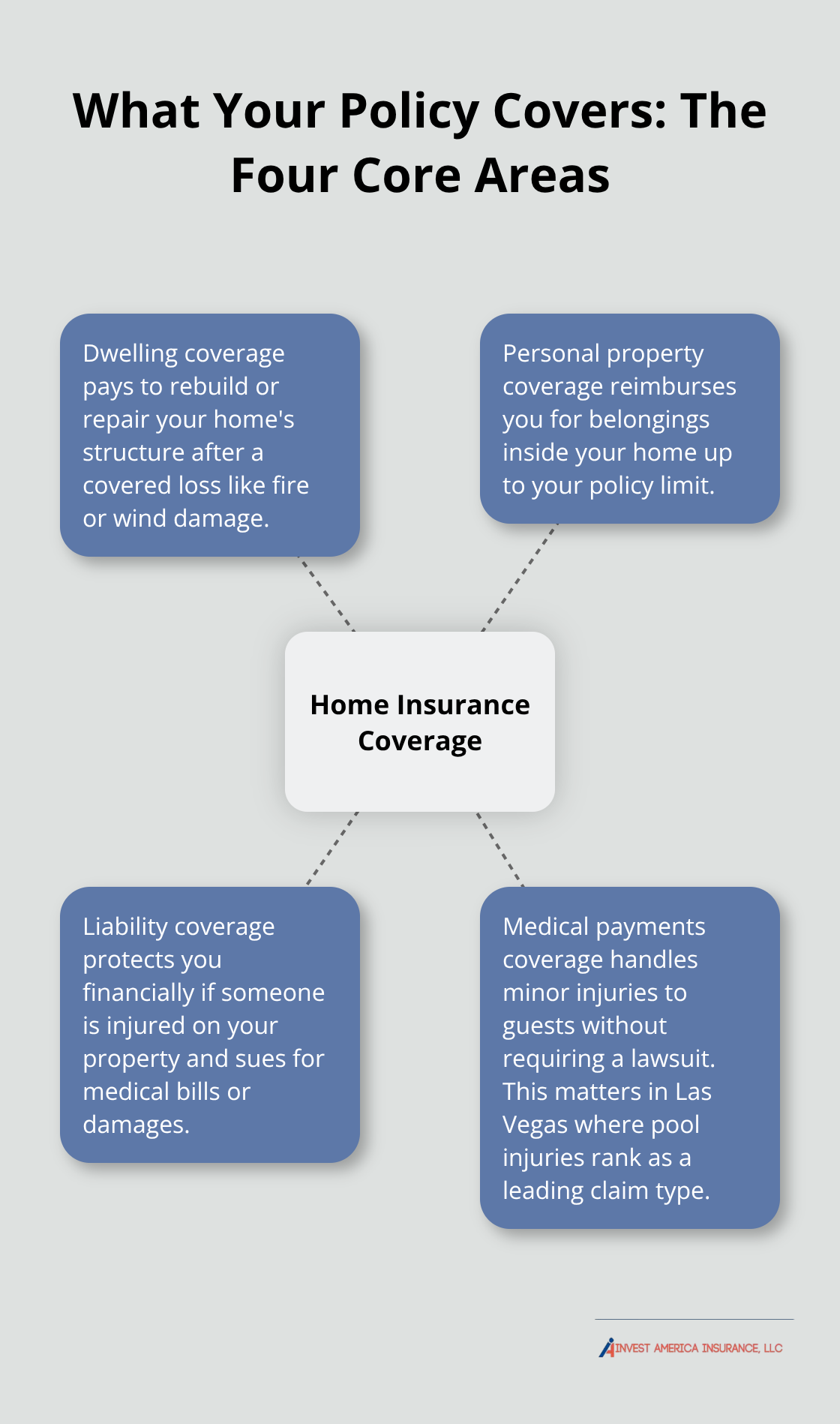

The Four Core Areas Your Policy Protects

Home insurance in Las Vegas protects four core areas of your property and finances. Dwelling coverage pays to rebuild or repair your home’s structure after a covered loss like fire or wind damage. Personal property coverage reimburses you for belongings inside your home-furniture, electronics, clothing-up to your policy limit. Liability coverage protects you financially if someone is injured on your property and sues you for medical bills or damages.

Medical payments coverage handles minor injuries to guests without requiring a lawsuit, which matters in Las Vegas where pool injuries rank as a leading claim type.

Critical Gaps: What Standard Policies Exclude

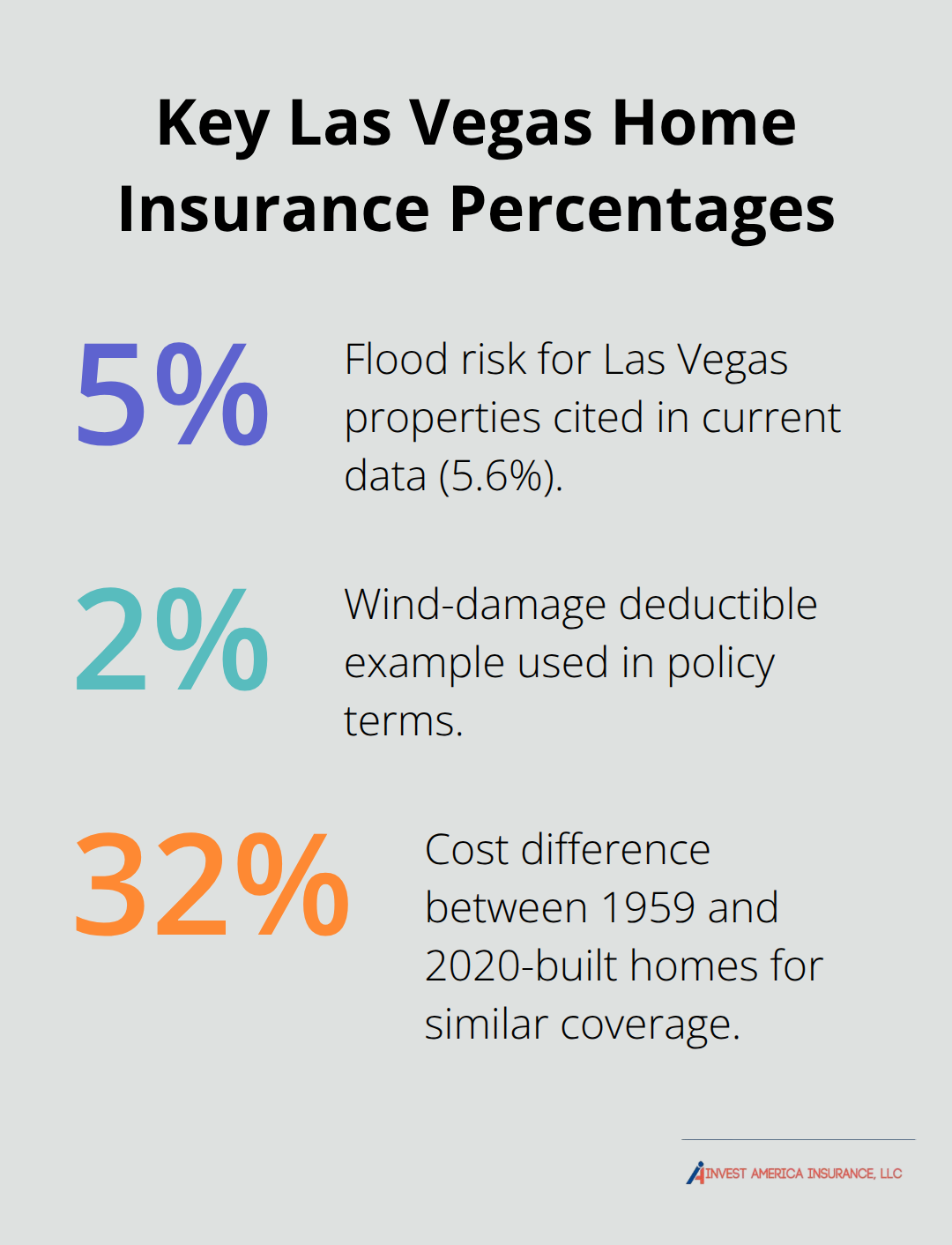

Standard policies exclude flood damage, earthquakes, and war-related losses. In Las Vegas, 5.6 percent of properties face flood risk according to current data, yet most homeowners skip flood coverage because they don’t understand this gap. Earthquake coverage also requires a separate endorsement, not a standard inclusion. If your home has a pool-common in Las Vegas-verify that your policy explicitly covers pool liability because standard coverage may have limits or exclusions specific to water features.

How Deductibles Shape Your Out-of-Pocket Costs

Your deductible is the amount you pay toward a claim before insurance kicks in, and it directly affects your monthly premium. Choosing a higher deductible lowers your premium but increases what you owe when you file a claim. With USAA in Las Vegas, moving from a $1,500 deductible to a $5,000 deductible can reduce annual premiums from roughly $846 to about $630-a meaningful difference over time. Some policies also use percentage-based deductibles for specific perils like wind damage. For example, with a $150,000 dwelling and a 2 percent wind-damage deductible, a $7,000 claim leaves you responsible for about $3,000 out-of-pocket. First-time buyers should set a deductible they can actually afford to pay if a loss occurs, not just chase the lowest premium.

Why Your Credit Score and Home Details Matter

Your credit score significantly influences your premium in Nevada. For the same $300,000 dwelling coverage with USAA, premiums range from about $2,695 with poor credit to $748 with excellent credit-more than a 260 percent difference. Home age also drives costs. A 1959-built home in Las Vegas costs roughly $1,125 annually with USAA for standard coverage, while a 2020-built home on the same policy runs about $853. Newer homes present lower fire and structural risk, so insurers reward them with better rates. Location within Las Vegas matters too. Homes near fire hydrants or fire departments qualify for better pricing because emergency response times are shorter. Construction material affects rates as well; brick construction costs less to insure than wood frame because brick resists fire and wind damage better than wood. When you shop for quotes, these factors will appear in your premium calculation, so understanding them helps you recognize fair pricing versus inflated rates.

Moving Forward: What to Examine Before You Compare Quotes

Before you request quotes from multiple carriers, inventory your belongings to understand how much personal property coverage you actually need. Calculate your home’s replacement cost-not its purchase price-because that number determines your dwelling limit. Identify any special features like pools, high-value art, or expensive jewelry that may require additional riders. These details shape which quotes make sense for your situation and which ones leave gaps in your protection.

Factors That Affect Your Home Insurance Rates

Location and Natural Disaster Risk Shape Your Premium Most

Location stands as the single biggest factor shaping your Las Vegas home insurance rate, and it matters far more than most first-time buyers realize. Nevada sits in an earthquake zone, and earthquake coverage requires a separate endorsement that costs extra. More immediately relevant to Las Vegas homeowners is flood risk. About 5.6 percent of Las Vegas properties face flood risk over the next 30 years, yet your standard policy won’t cover a penny of flood damage. If your home sits in a flood-prone area, you’ll need separate flood insurance through the National Flood Insurance Program or a private flood insurer, which adds $500 to $2,000+ annually depending on risk level.

Wildfire risk also influences pricing in Nevada. In 2023, insurers canceled or non-renewed roughly 1,475 policies due to wildfire exposure, showing how seriously carriers now treat this threat. Proximity to fire hydrants and fire departments actually lowers your premium because shorter emergency response times reduce loss severity. If your home is near a fire station or hydrant, mention this during quotes because many carriers offer discounts that don’t appear automatically. Construction material directly affects your rate as well. Brick construction costs substantially less to insure than wood frame because brick resists fire and wind damage far better. If you’re buying an older wood-frame home in a wildfire zone, expect higher premiums than a brick home blocks away.

Home Age Creates Striking Cost Differences

Home age is the second major cost driver, and the numbers are striking. A 1959-built home in Las Vegas costs roughly $1,125 annually with USAA for standard coverage, while a 2020-built home on the same policy runs about $853-a 32 percent difference for the same location and coverage. Older homes present greater fire risk, have outdated electrical systems that increase loss potential, and cost more to repair or rebuild because materials and labor have changed.

When comparing quotes on older homes, ask carriers if they offer discounts for recent roof replacements, electrical upgrades, or plumbing updates, because these improvements can materially lower your rate.

Credit Score and Claims History Drive Significant Rate Gaps

Your credit score in Nevada creates shockingly large rate differences. For the same $300,000 dwelling coverage with USAA, a borrower with poor credit pays roughly $2,695 annually while one with excellent credit pays $748-more than a 260 percent gap. Insurers use credit scores to predict claim likelihood and payment reliability, so if your credit is below 700, work on improving it before shopping for quotes. Even a 50-point improvement can save hundreds annually.

Claims history also matters if you’ve owned property before. Carriers track claims through a database, and multiple claims within five years signal higher risk. If you’ve filed claims previously, be transparent about them during the quote process because carriers will find them anyway, and honesty builds trust with your agent. First-time buyers have a clean slate here, which is an advantage-use it by maintaining a claims-free record going forward.

What This Means When You Shop for Quotes

These factors combine to shape the quotes you receive, and understanding them helps you recognize fair pricing versus inflated rates. A newer brick home near a fire station with excellent credit will pay substantially less than an older wood-frame home in a wildfire zone with fair credit-even if both homes sit in the same Las Vegas neighborhood. When you request quotes from multiple carriers, you’ll see these variables reflected in each premium. The next step involves comparing those quotes strategically and identifying which policies actually protect your specific situation rather than just chasing the lowest price.

Selecting the Right Policy for Your Situation

Calculate Your Dwelling Coverage Accurately

Start by calculating your actual dwelling coverage need, which is the estimated cost to completely rebuild your home from the foundation up, not what you paid for it. Many first-time buyers mistakenly use their purchase price, which often falls short of true replacement cost in Las Vegas where construction labor and materials have risen significantly. Request a replacement cost estimate from your agent or use online calculators that account for local Las Vegas construction costs. This number becomes your dwelling limit and forms the foundation of your entire policy.

Inventory Your Belongings and Set Personal Property Limits

For personal property coverage, inventory your belongings room by room and add up their value. This exercise reveals how much coverage you actually need rather than accepting a generic limit that may leave expensive items unprotected. Policies typically max out liability coverage around $500,000, but if you own a pool or host frequent guests, you should consider umbrella insurance to cover claims exceeding that limit. Pool ownership is extremely common in Las Vegas and represents a leading claim category, so explicit pool liability coverage becomes non-negotiable rather than optional. Once you know your dwelling limit, personal property total, and liability needs, you’re ready to request quotes that actually match your situation instead of generic quotes that leave gaps.

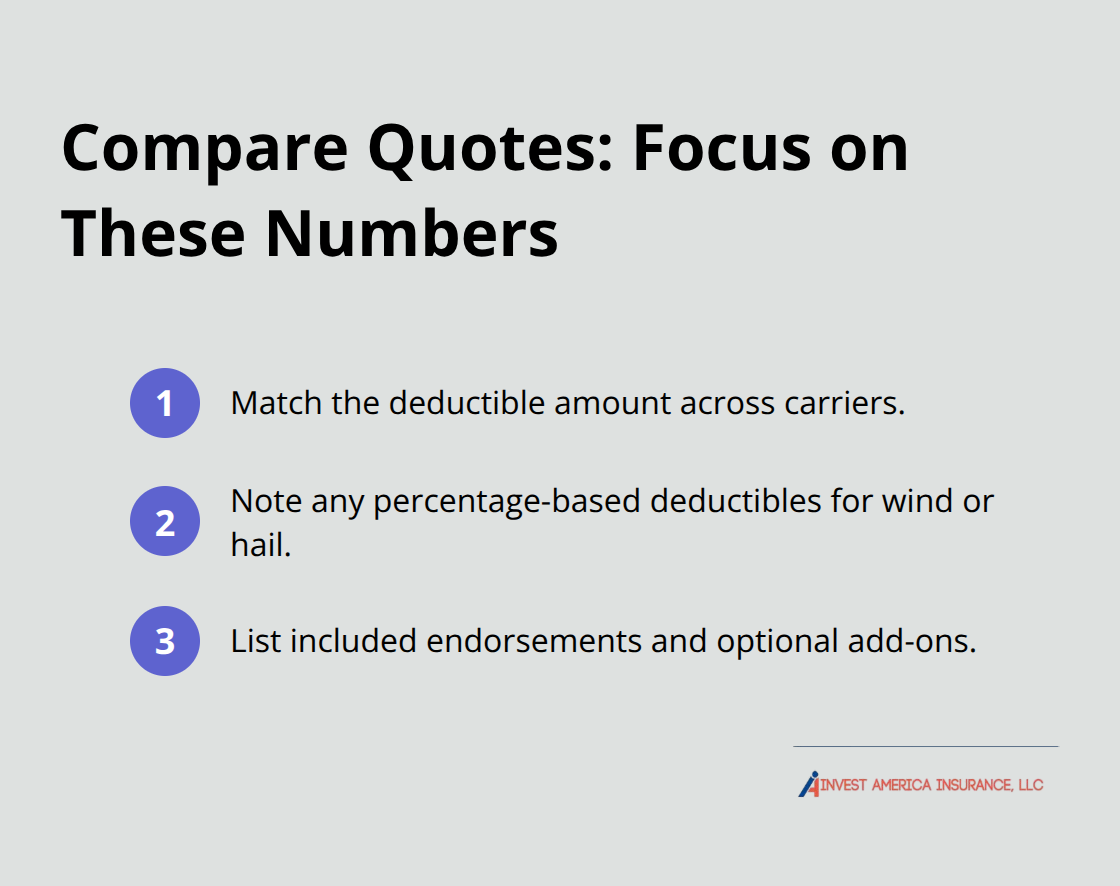

Compare Quotes on Identical Coverage Terms

When comparing quotes from multiple carriers, focus on three specific numbers beyond the premium: the deductible amount, any percentage-based deductibles for wind or hail damage, and the specific endorsements included or available. USAA, State Farm, and American Family consistently rank as top Las Vegas carriers, but eligibility varies significantly.

USAA restricts coverage to military members and families, State Farm offers strong policy management tools, and American Family excels at custom endorsements like water backup and equipment breakdown coverage. Las Vegas’s desert climate creates specific risks that matter more than generic coverage limits: water backup protection guards against flash floods and heavy rain damage, equipment breakdown coverage protects HVAC systems from sandstorm damage, and scheduled personal property riders protect high-value items like jewelry or electronics with sublimit concerns. Request quotes with identical coverage specifications from at least three carriers so you can directly compare apples-to-apples pricing rather than different coverage combinations that skew the comparison.

Identify Red Flags in Quotes and Carrier Responses

Red flags appear when a quote seems dramatically cheaper than others without explaining why, when an agent resists discussing exclusions or endorsements, when a carrier hasn’t asked about your home’s specific features like roof age or construction material, or when flood and earthquake coverage remain completely absent from the quote. An independent agency that represents multiple carriers can shop your specific needs across different companies rather than steering you toward a single insurer’s products. This approach saves time and typically reveals better pricing because agents can match your exact situation to the carrier offering the best rates for your profile rather than forcing you into a one-size-fits-all policy.

Final Thoughts

You now understand the core components of home insurance for first-time buyers: dwelling coverage protects your structure, personal property coverage protects your belongings, and liability coverage protects your finances if someone is injured on your property. Location, home age, and credit score drive your premium far more than most first-time buyers realize, and Las Vegas-specific risks like flood, wildfire, and pool liability demand explicit attention rather than assumptions about standard coverage. Start by calculating your dwelling replacement cost using local Las Vegas construction estimates, inventory your belongings to set personal property limits, and identify any special features like pools that require additional riders.

Request quotes from at least three carriers using identical coverage specifications so you can compare actual apples-to-apples pricing. Pay close attention to deductibles, percentage-based wind or hail deductibles, and available endorsements like water backup and equipment breakdown coverage that address desert climate risks. An independent agency that represents multiple carriers shops your specific situation across different companies and matches your exact needs to the carrier offering the best rates for your profile.

We at Invest America Insurance work with multiple top-rated carriers rather than being tied to any single company, which means we shop around on your behalf and offer coverage options tailored to your needs. Contact Invest America Insurance to get started with quotes that actually reflect your Las Vegas home and your specific situation. Your lender will require proof of coverage before closing, so starting early gives you time to compare options without rushing into a decision that leaves gaps in your protection.