Picking between term and whole life insurance is one of the biggest financial decisions you’ll make. The right choice depends on your budget, how long you need coverage, and your long-term goals.

At Invest America Insurance, we help Las Vegas residents understand these two fundamental options so you can protect your family without overpaying. This guide breaks down the differences to help you decide what works best for your situation.

How Term Life Insurance Works

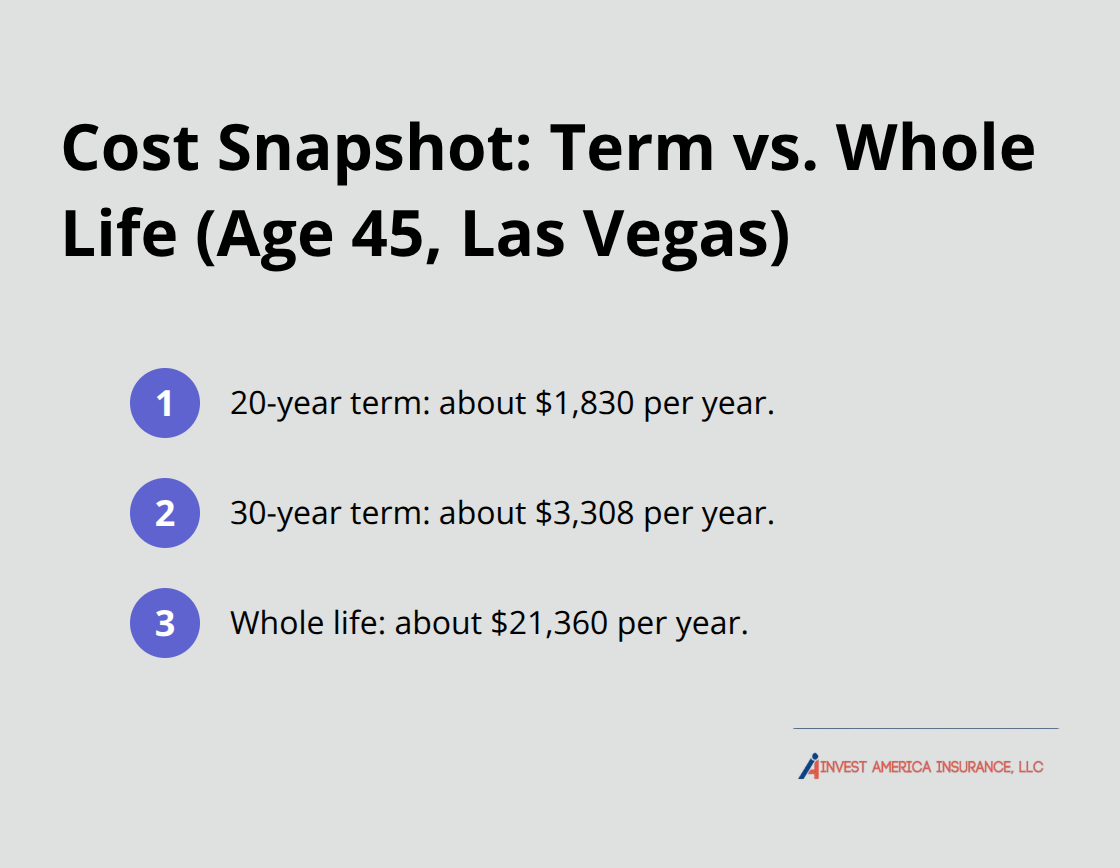

Term life insurance provides straightforward protection that covers you for a set number of years. If you die during that period, your beneficiaries receive the death benefit tax-free. The coverage ends when the term expires, which is why term policies cost significantly less than whole life options. A 45-year-old man in Las Vegas might pay around $1,830 per year for a 20-year term policy or $3,308 annually for 30 years, compared to roughly $21,360 yearly for whole life coverage. This popularity reflects that most people have specific financial obligations with defined timelines-paying off a mortgage, covering children until they graduate, or replacing income during peak earning years.

Term makes sense when you know exactly how long you need protection and want to minimize monthly costs.

Why Term Works for Your Timeline

Term policies come in multiple lengths, and the flexibility stands as one of their biggest advantages. You can lock in rates for 10, 15, 20, 30, or even 40 years, depending on the carrier and your situation. Banner Life, for example, offers 40-year terms that give you decades of affordable protection without building cash value. The key benefit is that your premium stays level throughout the entire term, so a policy you buy at age 35 will cost the same at age 55 if you chose a 20-year term. This predictability makes budgeting easier and protects you from rate increases. For Las Vegas residents, this stability matters-you lock in protection when you’re younger and healthier, which keeps your rates low. If your situation changes and you need permanent coverage later, many term policies include conversion options that let you switch to whole life without taking another medical exam (though conversion windows vary by insurer).

Death Benefit and Claims Reality

The death benefit provides pure protection with no additional complexity. If you pass away during the term, your beneficiaries receive the full amount tax-free, and they can use it however they need-paying off debt, covering funeral costs, replacing lost income, or funding education. The benefit amount stays level throughout the term, so a $500,000 policy pays exactly that if a claim occurs in year 1 or year 20. There’s no cash value component to manage, no loans to take out, and no surrender options to consider. This simplicity removes decision-making from your beneficiaries during an already difficult time. That protection proves particularly important during years when your family depends on your income most-when kids are young, a mortgage is active, or you’re the primary earner.

What Happens When Your Term Ends

When your term expires, your coverage ends unless you take action. You can renew the policy, but premiums will increase substantially because you’re older and the insurer adjusts rates accordingly. Alternatively, you can convert to a permanent policy (whole life, universal life, or indexed universal life) without a medical exam if your policy includes a conversion option. This conversion window typically lasts 10 to 15 years from the policy start date, though it varies by insurer. Conversion lets you lock in permanent coverage based on your health at the time of conversion, not your current health status. If you let the policy lapse without converting, you’ll need to reapply for new coverage and undergo medical underwriting again. For many Las Vegas residents, this flexibility makes term an ideal bridge-you get affordable protection now and can transition to permanent coverage later if your needs or financial situation changes.

What Whole Life Insurance Actually Covers

Whole life insurance works differently than term in almost every way that matters. Instead of coverage that expires, whole life stays with you for your entire life-up to age 121 according to most policies. Your premiums lock in at a fixed rate and never increase, which means a 45-year-old paying $21,360 annually will pay that same amount at 65, 75, or 85 if they keep the policy active. This permanence appeals to people who want lifetime protection without worrying about health changes or rate increases down the road.

How Cash Value Builds Inside Your Policy

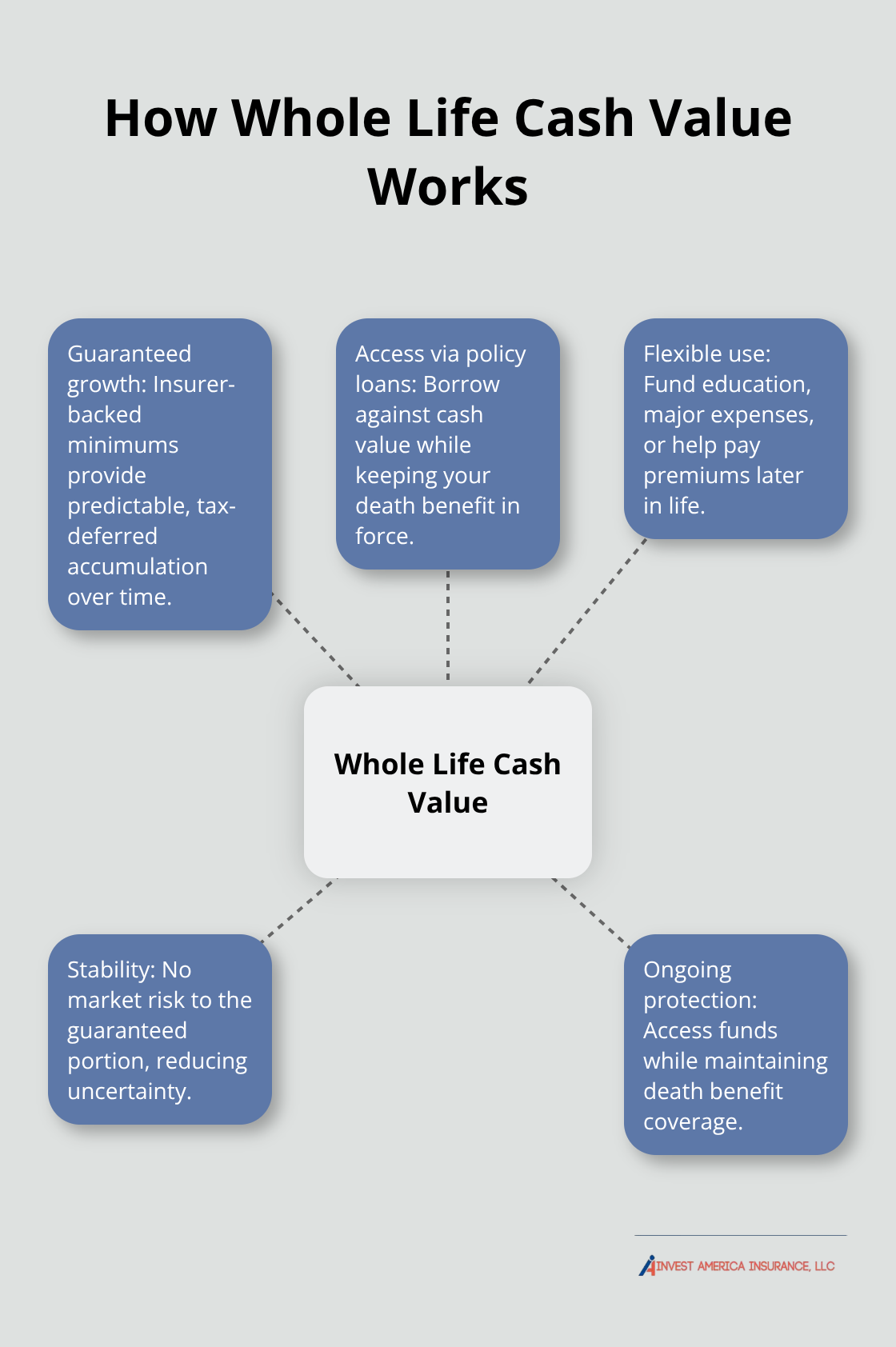

The real distinction between term and whole life is the cash value component that accumulates inside your policy. A portion of your premium funds a guaranteed cash value that grows tax-deferred over time. Unlike term life, which has zero value when it expires, whole life creates an actual asset you own. After 10 to 15 years, many policies accumulate enough cash value that you can borrow against it via policy loans, withdraw funds for education or major expenses, or use it to help pay premiums later in life. MassMutual, consistently rated as a top choice for whole life due to strong cash value growth, allows policyholders to access these funds while maintaining their death benefit protection. The growth rate is guaranteed by the insurance company, so you know exactly what your cash value will be at any given point-no market risk, no uncertainty.

Dividends and Paid-Up Additions

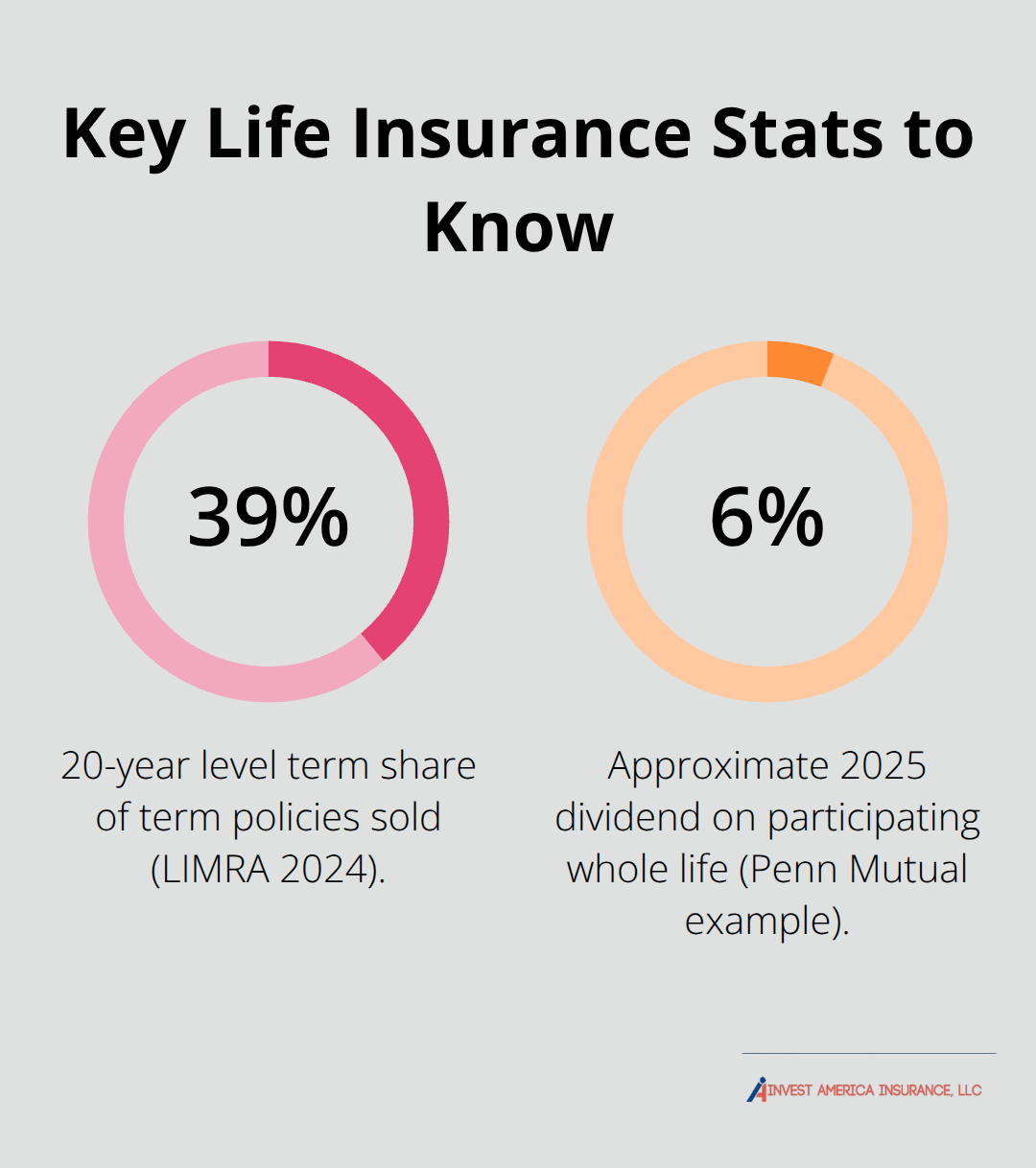

Participating whole life policies from mutual insurers can pay dividends based on company performance. Penn Mutual, for example, paid approximately 6 percent dividends in 2025 on participating policies, which accelerates cash value accumulation and can increase your death benefit through paid-up additions. These dividends aren’t guaranteed, but they reflect how mutual insurers share profits with policyholders when investment returns and claims experience are favorable. This matters practically: a Las Vegas resident buying whole life at 45 could see their cash value double or triple over 20 years depending on dividend performance, turning the policy into a genuine wealth-building tool rather than just protection.

The Cost Reality and Long-Term Value

The trade-off is obvious-whole life costs substantially more upfront. Where a 45-year-old man pays $1,830 yearly for 20-year term, that same person pays roughly $21,360 for whole life, or about 12 times more. However, that higher cost funds lifetime coverage plus an investment-like component with tax advantages that term cannot match. Research from The Ohio State University using Federal Reserve data found that households with both term and permanent life insurance were 5.58 times more likely to be financially prepared for income loss than those with no insurance at all. The combination strategy-starting with affordable term and adding whole life for long-term wealth building-addresses both immediate protection needs and future financial goals in ways that term alone cannot achieve.

Understanding whole life’s mechanics sets the stage for comparing these two options side by side. The next section examines the specific differences in cost, coverage length, and flexibility to help you determine which approach fits your financial situation.

Key Differences Between Term and Whole Life Insurance

The Cost Gap and What It Represents

The cost difference between term and whole life stands out immediately for Las Vegas residents, and understanding what that gap actually funds matters more than the raw numbers. A 45-year-old man buying a $500,000 policy pays roughly $1,830 annually for 20-year term coverage versus approximately $21,360 yearly for whole life according to Wealth Enhancement Group pricing data. That $19,530 annual difference adds up to roughly $400,000 over two decades. However, term provides pure death benefit protection that expires after 20 years, while whole life builds cash value and lasts your entire life. The premium difference funds not just lifetime coverage, but an asset you can access, borrow against, or pass to heirs. For Las Vegas families, this means choosing between minimal out-of-pocket cost now versus building long-term financial flexibility later. If your primary goal is income replacement during peak earning years when kids are young and a mortgage exists, term delivers protection at a fraction of the cost. If you want to protect your family indefinitely while simultaneously building accessible wealth, whole life justifies its higher price tag through guaranteed cash value growth, potential dividends, and tax-free policy loans.

Coverage Length and Timeline Considerations

Term policies expire at predetermined points-typically after 10, 20, 30, or 40 years-which means you must plan around that expiration date or face losing protection when you need it most. A 35-year-old who buys 30-year term coverage reaches age 65 with no insurance if they don’t convert or renew, precisely when final expense costs and legacy planning matter. Whole life eliminates this timeline problem because coverage continues until death, with fixed premiums that never increase regardless of health changes or age. According to LIMRA’s 2024 data, the 20-year level term dominates the market at 39 percent of all term policies sold, suggesting most buyers align coverage with mortgage payoff or children’s college graduation. This creates a planning gap: what happens at expiration?

Conversion options available on many term policies allow switching to permanent coverage without medical exams, but the conversion window typically closes 10 to 15 years from purchase.

Cash Value: The Defining Feature

Cash value separates these products fundamentally-term has none, while whole life cash value grows at a guaranteed minimum rate and can be borrowed against while maintaining your death benefit. A Las Vegas resident age 45 who purchases whole life might access $50,000 in cash value by age 55 and substantially more by retirement, creating a tool for funding education, managing debt, or supplementing retirement income. Term policies simply expire with zero remaining value, making them pure protection rather than wealth-building vehicles. MassMutual, consistently rated as a top choice for whole life due to strong cash value growth, demonstrates how this component transforms insurance into a financial asset. Participating whole life policies from mutual insurers can pay dividends based on company performance, which accelerates cash value accumulation and can increase your death benefit through paid-up additions. These dividends aren’t guaranteed, but they reflect how mutual insurers share profits with policyholders when investment returns and claims experience are favorable.

Real-World Financial Preparedness

Research from The Ohio State University using Federal Reserve data found that households with both term and permanent life insurance were 5.58 times more likely to be financially prepared for income loss than those with no insurance at all. The combination strategy-starting with affordable term and adding whole life for long-term wealth building-addresses both immediate protection needs and future financial goals in ways that term alone cannot achieve. This dual approach lets you lock in affordable protection during your peak earning years while building an asset that serves you throughout retirement.

Final Thoughts

Your choice between term vs whole life insurance depends on three factors: how long you need coverage, what you can afford monthly, and whether building cash value matters to your long-term financial plan. If you’re a Las Vegas resident with young children, an active mortgage, and limited discretionary income, term life delivers the protection your family needs at a price that fits your budget. A 20 or 30-year term aligns with major financial obligations and keeps premiums manageable during peak earning years.

If you want lifetime protection that never expires and you value the ability to access cash value for future needs, whole life provides permanent coverage with guaranteed growth and potential dividends that term cannot match. Start by calculating how much coverage you actually require-most financial advisors recommend coverage equal to 8 to 10 times your annual income, though your specific number depends on outstanding debt, dependent care costs, and income replacement goals. Next, determine your timeline honestly by asking when your children will graduate, when you plan to retire, and when your mortgage will be paid off.

At Invest America Insurance, we work with multiple top-rated carriers to find coverage that matches your needs and budget. As an independent agency based in Las Vegas, we shop around on your behalf rather than pushing a single company’s products, and we help you compare actual quotes side by side to select the right policy for your situation. Contact us today to discuss your options and get protected with coverage that actually fits your life.