Homeowners in Las Vegas face unique insurance costs shaped by the desert climate, urban growth, and local risk factors. Understanding the average cost of home insurance in Las Vegas helps you budget properly and identify savings opportunities.

We at Invest America Insurance know that many residents overpay simply because they haven’t compared quotes or explored available discounts. This guide breaks down what you’ll actually pay and how to reduce your premiums.

What Las Vegas Homeowners Actually Pay

Monthly and Annual Costs for Las Vegas Residents

The average cost of homeowners insurance in Las Vegas runs about $1,103 to $1,304 per year for a $300,000 dwelling, depending on your specific profile and carrier. That breaks down to roughly $92 to $109 monthly.

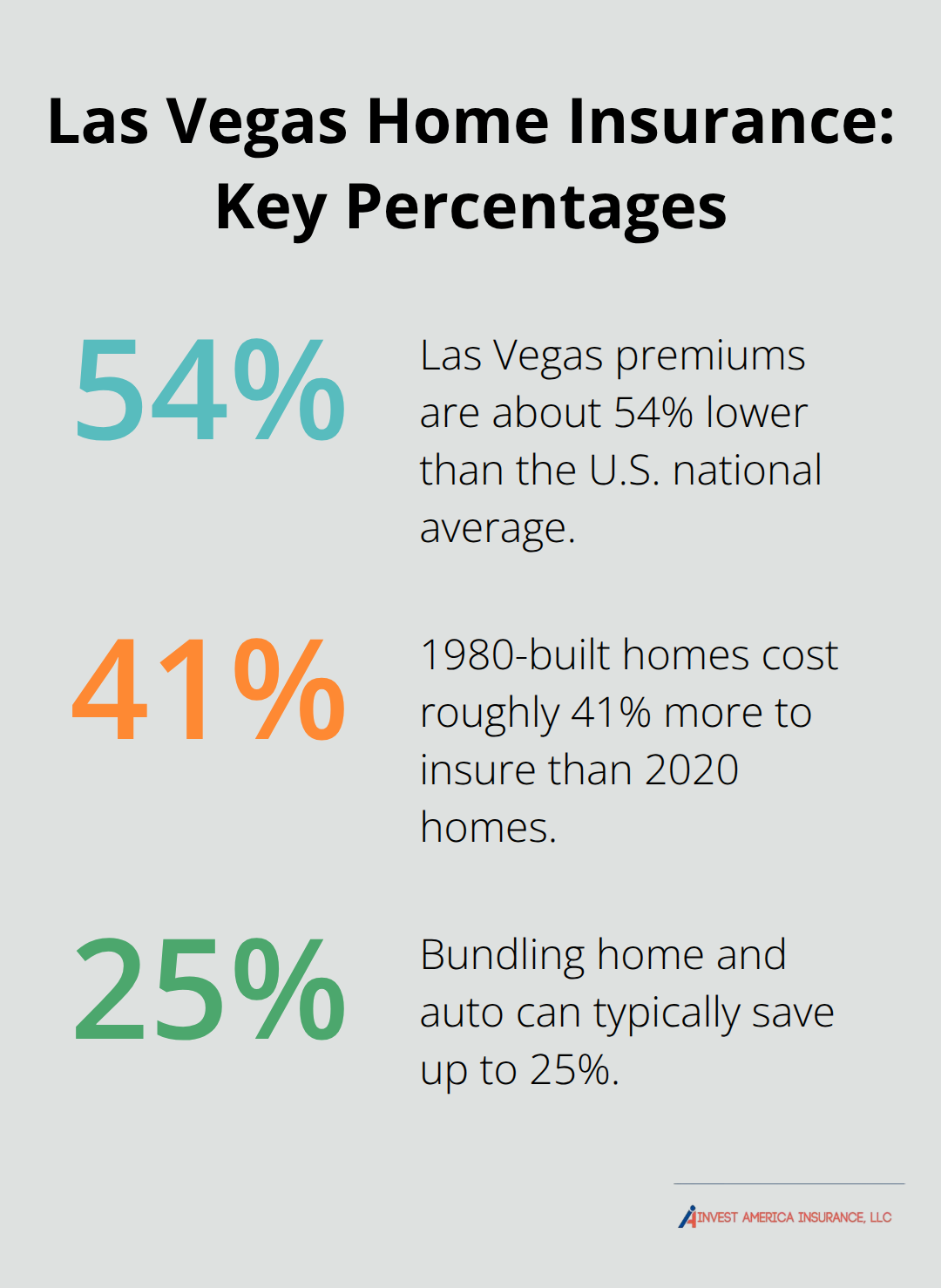

According to Bankrate’s November 2025 data, Las Vegas sits slightly above Nevada’s statewide average of $1,074 annually, but here’s what matters: Las Vegas premiums are about 54% lower than the national average, making your desert home far more affordable to insure than properties in high-risk coastal or tornado-prone states.

Nearby cities show similar pricing. Henderson averages around $989 yearly, Reno about $964, and Sparks approximately $947, so you’re not paying an unusual premium just for living in Las Vegas proper. The gap between the cheapest and most expensive carriers is substantial though. USAA (limited to military members and families) quotes around $958 annually for $300,000 coverage, while American Family runs closer to $1,326 for the same dwelling amount according to Bankrate data. State Farm falls in the middle at roughly $1,095.

What Shapes Your Individual Premium

Your actual premium depends heavily on three things: the home’s age, your credit score, and your deductible choice. A 1959-built home costs roughly 32% more to insure than a 2020-built home with USAA-about $1,125 versus $853 annually. Credit score creates an even sharper divide: excellent credit averages $827 yearly while poor credit jumps to $2,485, according to MoneyGeek’s analysis.

Raising your deductible from $500 to $1,500 or $2,000 can cut premiums by roughly $200 to $220 annually; pushing it to $5,000 saves even more, around $216 per year with USAA. MoneyGeek’s data confirms similar ranges across carriers, with Capital Insurance Group offering the lowest statewide premiums around $672 yearly, while COUNTRY Financial reaches $1,626 for comparable coverage.

Why Las Vegas Rates Stay Competitive

Nevada’s desert climate is your advantage. The state experiences only about 0.6 severe weather events annually according to NOAA data, far fewer than hurricane-prone or tornado-heavy states where premiums routinely exceed $4,000 yearly. Las Vegas doesn’t face the wildfire exposure that drives California rates to $1,641 on average, nor the hail damage risk that pushes Oklahoma to $4,695.

However, 2025 brought rising pressure. Premiums surged statewide due to extended drought fueling wildfires, increased flash-flooding incidents, construction costs climbing sharply, and insurers’ reinsurance expenses rising. Nevada’s growing population, especially around Las Vegas, has also expanded insurer exposure. Rising labor and material costs mean rebuild estimates-not market value-now determine your premium, so even if your home’s resale price stayed flat, your insurance cost likely climbed.

How to Find Your Real Cost

The only way to know your real cost is to collect quotes from multiple carriers. Bankrate’s baseline profile (40-year-old married homeowners, 2017 build, good credit, $300,000 dwelling, $1,000 deductible) shows significant variation among carriers, and your situation will differ. A home built in 1980 costs about 41% more to insure than one from 2020. Filing even one claim adds roughly $200 to your annual premium for five years.

When you compare quotes, check the financial strength ratings from AM Best and customer satisfaction scores from JD Power-price alone doesn’t tell the full story. Obtain at least three quotes side-by-side, comparing not just premium but claims handling reputation and coverage flexibility. Understanding these cost drivers positions you to make smarter choices about which coverage levels and deductibles actually fit your budget and risk tolerance.

What Actually Drives Your Las Vegas Home Insurance Premium

Replacement Cost Sets Your Premium, Not Market Value

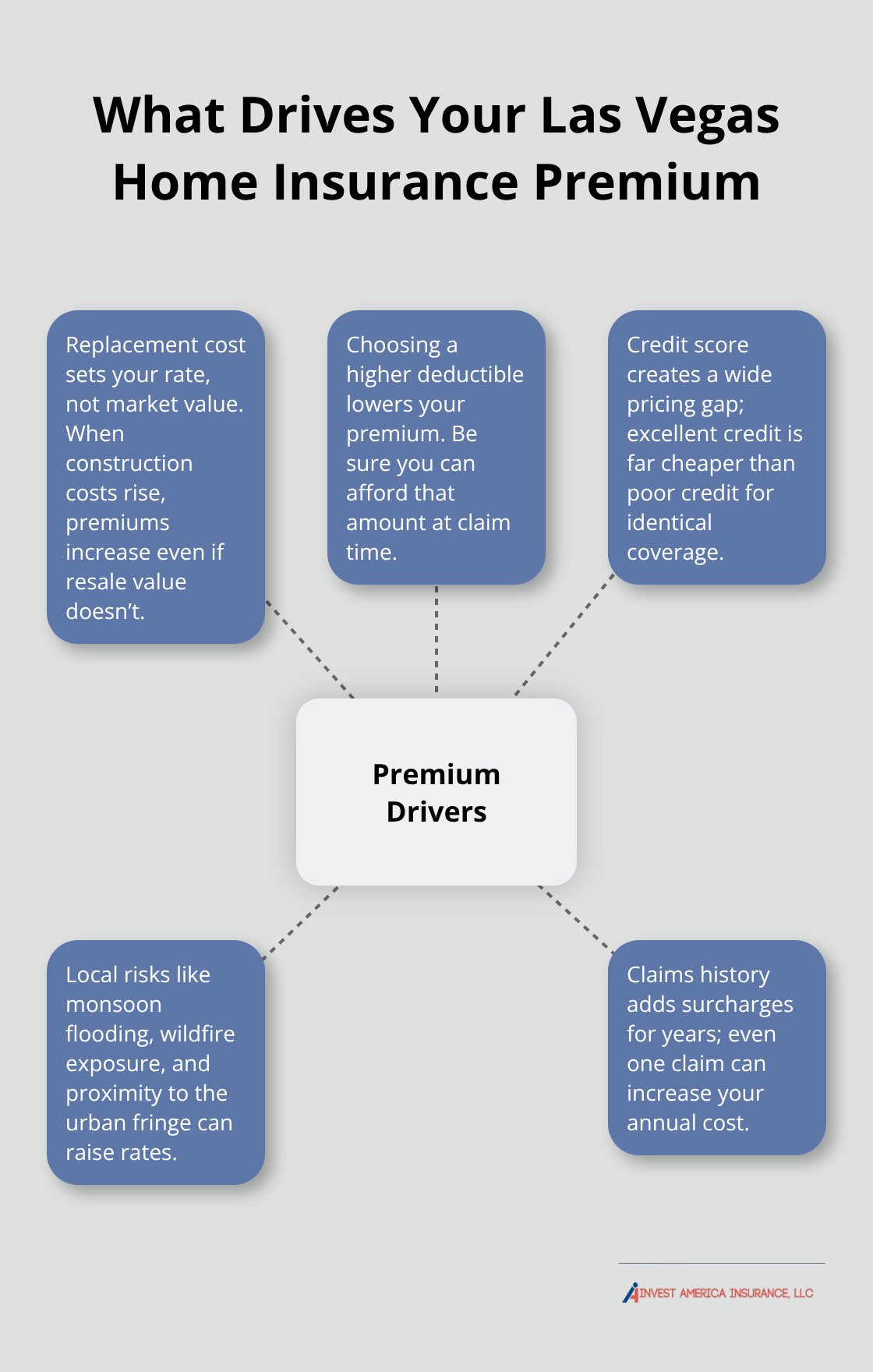

Replacement cost is the cost necessary to repair or replace your entire home, and it determines your premium, not your home’s market value. This distinction matters enormously. A Las Vegas home worth $400,000 might cost $350,000 to rebuild using current lumber, steel, and labor rates. Insurers focus on that $350,000 replacement figure.

When construction costs spike-as they did throughout 2024 and 2025-your premium climbs even if your home’s resale price remains unchanged. Homes built in 1980 cost roughly 41% more to insure than identical 2020 homes because older properties require more work to bring up to current building codes during reconstruction, according to MoneyGeek analysis.

Your Deductible Choice Directly Impacts Your Monthly Bill

Raising your deductible from $500 to $1,000 saves about $91 annually. Pushing it to $2,000 or $5,000 creates even sharper reductions-USAA customers who select a $5,000 deductible pay roughly $630 annually versus $846 for a $1,500 deductible. The trade-off is straightforward: higher deductible means lower premium, but you must be able to actually pay that amount if a claim occurs. This decision shapes your long-term costs more than most people realize.

Credit Score Creates a Dramatic Premium Gap

Your credit score matters more than most people realize. MoneyGeek’s Nevada data reveals that excellent credit yields premiums around $827 yearly while poor credit reaches $2,485 for identical coverage-a $1,658 annual gap. This three-fold difference exists because insurers view credit history as predictive of claims behavior and financial responsibility. Improving your credit score before shopping for insurance can unlock substantial savings.

Las Vegas Location Introduces Specific Risk Layers

Monsoon season brings flash-flooding risk, particularly in certain neighborhoods and ZIP codes; water backup coverage costs extra but protects against basement flooding during heavy storms. Wildfire exposure has intensified as drought conditions persist across Nevada, pushing some carriers to require additional mitigation measures or adjust rates accordingly. Your home’s proximity to the urban fringe matters too-properties closer to undeveloped areas face higher wildfire exposure than central Las Vegas homes. Neighborhood property values also influence rates; wealthier ZIP codes with higher home concentrations naturally carry higher liability exposure.

Claims History Permanently Affects Your Premium Trajectory

Filing a claim permanently affects your premium trajectory. One claim adds approximately $200 to your annual cost for five consecutive years, according to MoneyGeek data. Two claims jump that surcharge to roughly $368 yearly for the same period. This means a water damage claim today costs you $1,000 in extra premiums over five years, making it worth considering your deductible threshold carefully before filing minor claims. When comparing quotes, your coverage limits matter as much as your deductible. A $300,000 dwelling limit with $100,000 personal property and $300,000 liability generates a baseline premium. Bumping to $500,000 dwelling and $250,000 personal property increases costs substantially. Las Vegas residents with pools, frequent entertaining, or valuable collections should consider higher liability limits or umbrella policies; the premium increase for additional liability is minimal compared to the protection it provides. Understanding these cost drivers positions you to make smarter choices about which coverage levels and deductibles actually fit your budget and risk tolerance-and that knowledge becomes essential when you start shopping for actual quotes from carriers.

Reduce Your Premium Without Sacrificing Coverage

Compare Quotes Across Multiple Carriers

Comparing quotes from different carriers should be your first move, not your last resort. Homeowners who request three quotes often discover they could save $200 to $400 annually without changing coverage. Compare quotes from different carriers with USAA, State Farm, and American Family, which offer some of the best cheap home insurance in Las Vegas according to Bankrate’s research.

You need actual quotes from your specific carriers, not ballpark estimates, because rates vary dramatically by ZIP code and individual profile. When you obtain quotes, compare the same coverage limits across carriers: $300,000 dwelling, $100,000 personal property, and $300,000 liability gives you an apples-to-apples baseline. Check the financial strength ratings from AM Best and customer satisfaction scores from JD Power while you compare prices, because a $50 monthly savings means nothing if the carrier denies your claim or takes months to process it.

Bundle Policies to Unlock Immediate Savings

Bundling home and auto policies typically saves 10 to 25 percent according to industry data, yet many Las Vegas homeowners maintain separate policies with different carriers. If you carry auto insurance elsewhere, moving your homeowners policy to that same carrier often qualifies you for a multi-policy discount immediately. Some carriers offer additional discounts for bundling home, auto, and umbrella coverage together-savings that compound quickly.

Install safety features that carriers actually reward: monitored security systems, smoke detectors, and deadbolt locks typically reduce your premium by a measurable percentage. Ask your carrier specifically which upgrades qualify for discounts before you spend money on improvements; some carriers offer discounts for newer roofs or upgraded electrical systems, while others don’t. Maintain a claim-free history to position yourself for loyalty discounts when you renew. If you’ve been with the same carrier for multiple years, ask directly about retention discounts during renewal; many carriers offer 5 to 10 percent reductions for long-term customers, but you must ask.

Adjust Your Deductible to Match Your Budget

Raising your deductible from $500 to $1,000 saves approximately $91 annually; pushing it to $2,000 saves roughly $200 yearly. The catch is ensuring you can actually pay that deductible if a claim occurs, so don’t raise it beyond what you can afford immediately. This decision shapes your long-term costs more than most people realize.

The trade-off is straightforward: higher deductible means lower premium, but you must have the cash available if a claim happens. Consider your emergency fund and financial situation before you commit to a higher deductible threshold.

Add Coverage That Protects Against Local Risks

Water backup coverage costs extra but protects against basement flooding during Las Vegas monsoon season, and it’s worth the modest premium increase if you have a basement or live in a flood-prone ZIP code. Las Vegas has a relatively minor flood risk with about 5.6 percent of properties at risk over the next 30 years, but if your home falls in that percentage, the coverage pays for itself after one claim.

Older homes cost roughly 41 percent more to insure than newer ones because rebuilding an older structure requires bringing it up to current building codes. If you own a 1980-built home, modest updates-upgraded electrical wiring, roof repairs, or plumbing improvements-can reduce your rebuild estimate and lower your premium. Document these improvements and notify your carrier; some may adjust your premium downward if the work improves the home’s condition.

Final Thoughts

Las Vegas homeowners pay between $1,103 and $1,304 annually for a $300,000 dwelling, placing your desert home roughly 54 percent below the national average. That affordability stems from Nevada’s low severe-weather frequency and lack of hurricane exposure, but 2025 brought rising costs driven by construction inflation, wildfire risk, and increased flood incidents. Your actual premium depends far more on replacement cost, credit score, home age, and deductible choice than on market value alone-a home built in 1980 costs 41 percent more to insure than a 2020 home, and excellent credit saves you $1,658 annually compared to poor credit.

Finding affordable coverage requires three concrete steps: collect quotes from at least three carriers and compare identical coverage limits side-by-side while checking AM Best financial ratings and JD Power satisfaction scores alongside price, bundle your home and auto policies to unlock 10 to 25 percent savings immediately, and adjust your deductible to match your budget while adding water backup coverage if you live in a flood-prone ZIP code. An independent agent represents your interests rather than a single carrier’s agenda, shopping multiple top-rated carriers on your behalf and tailoring coverage to your specific needs and budget. They explain coverage details clearly, help you navigate claims, and adjust your policy as your situation changes.

When you’re ready to find the right coverage for your Las Vegas home, contact Invest America Insurance to compare quotes from multiple carriers and discover the average cost of home insurance in Las Vegas that actually fits your financial situation.