Most Las Vegas families struggle with the question: how much life insurance do I need? The answer depends on your income, debts, and dependents.

We at Invest America Insurance see this confusion daily. Getting the right coverage amount protects your family’s financial future without overpaying for unnecessary protection.

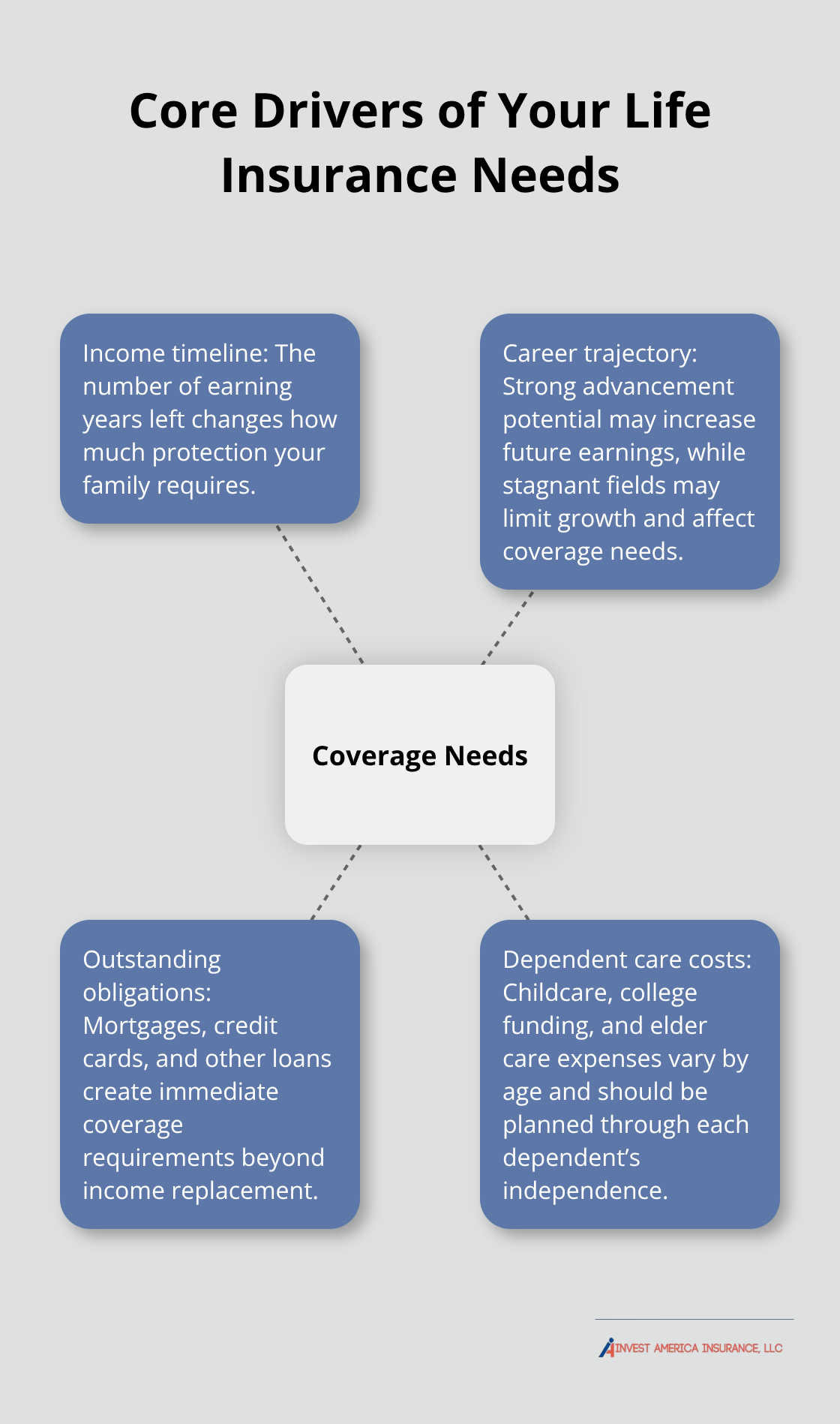

What Factors Shape Your Life Insurance Needs

Three financial realities determine your life insurance requirements, and insurance professionals examine these first. Your current salary provides the foundation, but your career path holds greater importance. A 30-year-old teacher who earns $45,000 annually with strong advancement potential requires different coverage than someone in a declining industry. Career earnings vary dramatically by profession, with some fields experiencing significant income growth over time while others face stagnant wages.

Your Income Replacement Timeline

Most financial planners recommend 10-12 times your annual income, but this generic formula fails Las Vegas families. A construction worker who earns $65,000 might need only 8 times income due to shorter dependency periods, while a casino manager with young children requires 15 times to cover college costs and extended family support. Your remaining earning years directly impact this calculation. Someone with 30 working years ahead needs more coverage than someone five years from retirement.

Outstanding Financial Obligations

Your mortgage, credit cards, and loans create immediate coverage needs that income replacement formulas miss. Las Vegas homeowners face significant mortgage obligations that must be considered in coverage calculations. Add typical consumer debt, and you need substantial coverage before considering family living expenses. High-interest debt like credit cards should receive priority coverage since these payments continue even after death and drain survivor benefits quickly.

Dependent Care Costs

Each dependent adds specific financial requirements that change with age. Childcare for infants requires substantial annual investment in Las Vegas, while teenage dependents need college funding for future education costs. Elderly parents who require care add another layer, with assisted living facilities representing a significant monthly expense. Calculate these costs through each dependent’s expected independence age, not just current expenses.

These factors work together to create your baseline coverage needs, but the calculation method you choose can significantly impact your final coverage amount.

How Do You Calculate Life Insurance Coverage

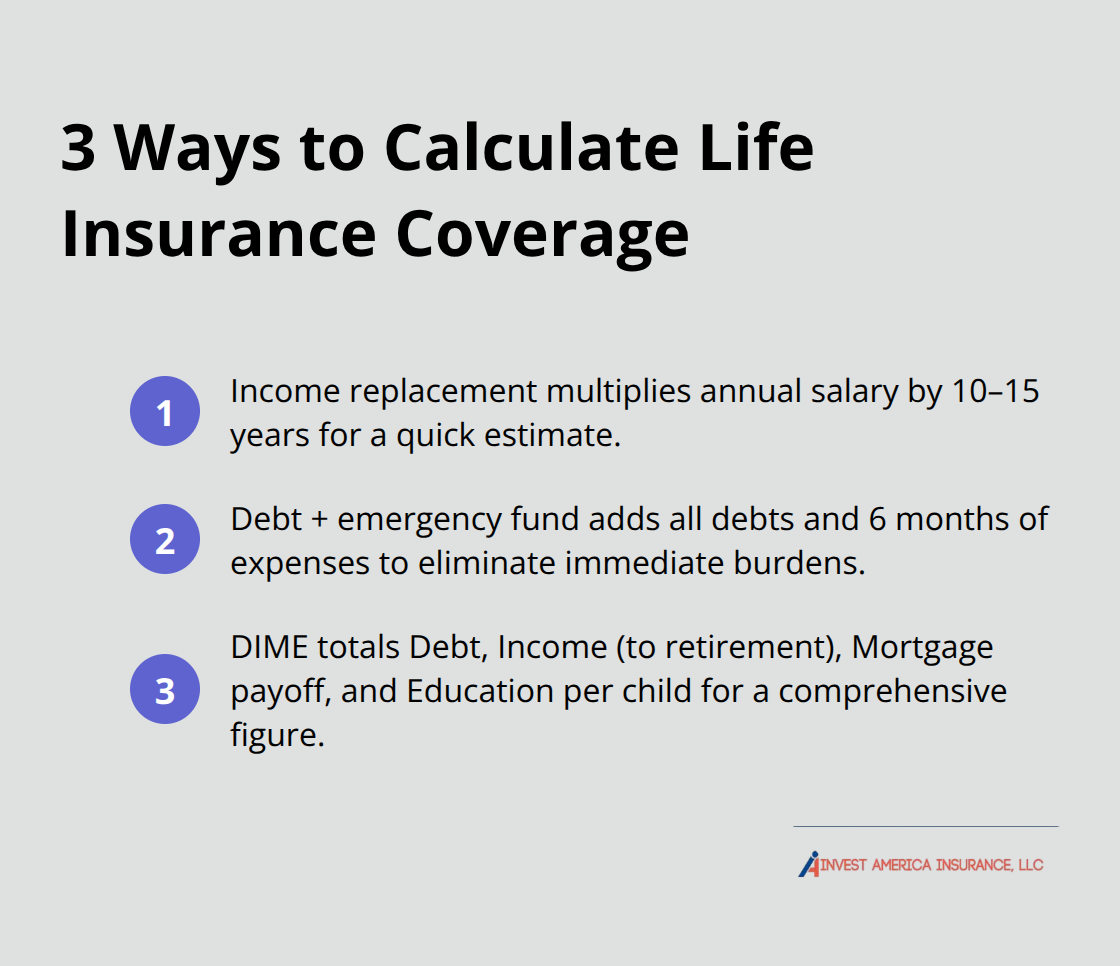

Three calculation methods dominate the insurance industry, and each serves different financial situations. The income replacement method multiplies your annual salary by 10-15 years and provides straightforward calculations that most Las Vegas families can handle independently. Financial advisors typically recommend 10 times income for younger workers with decades of earning potential, while those closer to retirement need only 7-8 times their current salary. This method works best for steady earners but fails families with irregular income or significant debt burdens.

Income Replacement Method for Working Families

This approach focuses on your salary and career timeline to determine coverage needs. Multiply your current income by the number of years your family needs financial support. A 35-year-old casino dealer who earns $55,000 annually might need $550,000 in coverage (10 times income) to support dependents through college years. Workers in stable industries with predictable raises can use lower multipliers, while those in volatile fields should consider higher ratios. The method assumes your family can invest the death benefit and live off investment returns.

Debt Coverage Plus Emergency Fund Strategy

Smart families start with total debt elimination, then add emergency funds for comprehensive protection. Calculate your mortgage balance, credit card debt, student loans, and car payments for the foundation amount. Las Vegas homeowners typically carry substantial mortgage debt according to recent market data, which requires substantial base coverage before income replacement considerations. Add six months of expenses as an emergency buffer (typically $30,000-45,000 for middle-income families). This approach protects survivors from financial stress while providing time for major decisions.

DIME Method for Comprehensive Planning

The DIME formula addresses Debt, Income, Mortgage, and Education expenses through systematic calculation. Add all debts, multiply income by years until retirement, include mortgage payoff amounts, and estimate education costs for each child. College expenses vary significantly for Nevada residents, which means substantial planning per child for four-year degrees. This method produces higher coverage amounts but addresses real financial obligations that basic income replacement misses. Most families need $500,000-750,000 with DIME calculations.

Each method produces different coverage amounts, and the type of life insurance you choose affects how much protection you can afford.

Which Life Insurance Type Fits Your Coverage Needs

Term life insurance provides maximum coverage for families who need substantial protection on limited budgets, which makes it the smart choice for most Las Vegas households. A healthy 35-year-old can secure $500,000 in 20-year term coverage for approximately $30-40 monthly, while comparable whole life insurance costs $300-400 per month according to recent industry data. Term policies work perfectly for temporary needs like mortgage protection and child expenses that disappear over time. The coverage expires when your financial obligations typically decrease, such as when children become independent and mortgages reach completion.

Term Life Insurance Provides Affordable Protection

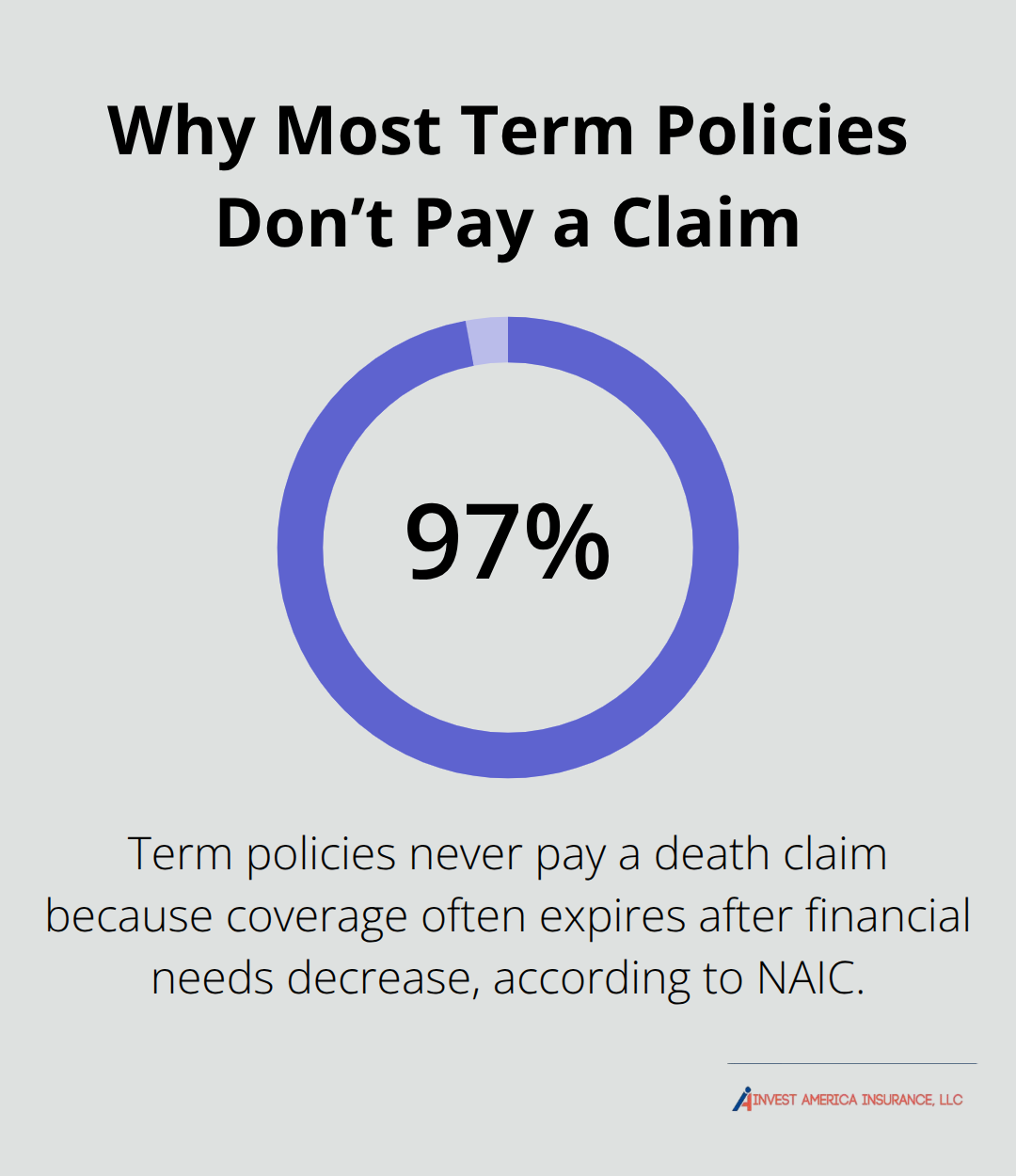

Term coverage costs 10-15 times less than permanent insurance, which means families can afford adequate protection during peak years. Most Las Vegas families need $500,000-750,000 in coverage based on DIME calculations, but permanent insurance at these amounts creates unaffordable premiums for middle-income earners. Term insurance allows you to buy sufficient coverage now and invest the premium difference in retirement accounts or other investments. The National Association of Insurance Commissioners reports that 97% of term policies never pay claims because coverage expires after financial needs decrease (this represents successful financial planning rather than wasted premiums).

Whole Life Insurance Builds Cash Value

Whole life insurance combines death benefits with forced savings accounts that grow through guaranteed cash values and dividends. These policies cost significantly more but provide permanent coverage that never expires, plus cash access through loans or withdrawals. Whole life makes sense for estate plans when you need guaranteed death benefits regardless of age, or for high-income earners who maximize other tax-advantaged accounts. The cash value grows slowly in early years, typically takes 15-20 years to exceed total premiums paid, which makes this inappropriate for families who need maximum death benefit protection.

Universal Life Insurance Offers Premium Flexibility

Universal life policies allow premium adjustments and coverage changes while they build cash value through market investments or guaranteed interest rates. These policies work for business owners with income fluctuations who need flexible premium payment schedules. However, universal life requires active management since insufficient premiums can cause policy lapses, and market performance directly affects cash value growth. Most families benefit more from term insurance combined with separate investment accounts rather than complex universal life structures (which require constant monitoring and adjustment).

Final Thoughts

Life insurance needs shift as your financial situation evolves, so annual reviews protect your family from coverage gaps or overpayment. Marriage, new children, home purchases, and career changes all impact how much life insurance you need. Most Las Vegas families benefit from annual coverage reviews alongside tax planning and retirement contributions.

Licensed insurance professionals save time and money through proper coverage analysis and carrier comparisons. We at Invest America Insurance help families find competitive rates that fit their specific needs and budget. Independent agents compare policies across companies rather than sell single-carrier products (which limits your options and potentially increases costs).

Term life insurance provides the best starting point for most families who need substantial coverage at affordable rates. You can always add permanent insurance later when your income increases and basic protection needs are met. Las Vegas families can get quotes from multiple carriers to find the right coverage amount and premium structure for their situation.