Running a small business in Nevada means facing real liability risks every single day. One accident or injury on your property could lead to a lawsuit that threatens your entire operation.

General liability insurance in Nevada protects your business from these financial disasters. At Invest America Insurance, we help Nevada business owners understand exactly what coverage they need and how to get it at the right price.

What General Liability Insurance Actually Covers

Third-Party Claims Protection

General liability insurance protects your Nevada business from the financial fallout of third-party claims-meaning injuries or damage involving someone other than you or your employees. If a customer slips on your floor and breaks their leg, or your equipment damages a client’s property, general liability steps in to cover medical bills, repair costs, and legal expenses. The Hartford, the top-rated general liability insurer in Nevada with a MoneyGeek score of 4.64 out of 5, offers limits ranging from $300,000 to $2,000,000 per occurrence, allowing you to match your coverage to your actual exposure.

Coverage Limits That Match Your Business

Most Nevada small businesses choose $1 million per occurrence and $2 million aggregate limits because these thresholds meet typical contract requirements and protect against the slip-and-falls, property damage incidents, and advertising injuries (like slander or libel claims) that happen in day-to-day operations. Your policy also covers legal defense costs, which can run into tens of thousands of dollars before a case even reaches trial. This protection matters whether you operate a retail storefront, a service business, or a contractor operation-the liability exposure remains real across all industries.

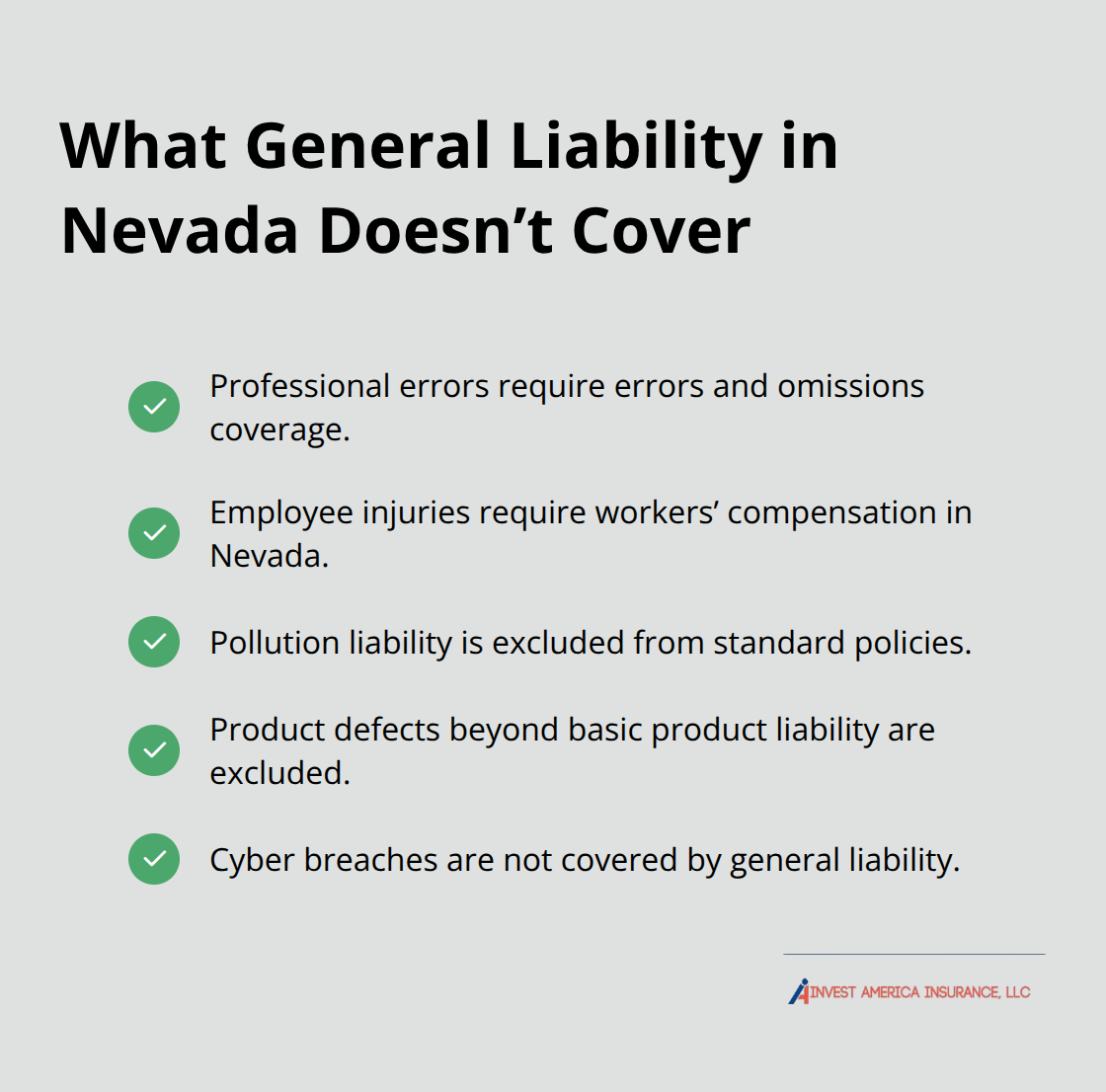

What General Liability Does Not Cover

Professional errors fall outside standard general liability coverage. If you’re an accountant and miscalculate a client’s taxes, or a consultant gives bad advice, you need separate errors and omissions coverage.

Employee injuries require workers’ compensation, which in Nevada applies to businesses with four or more employees. Pollution liability, product defects beyond basic product liability, and cyber breaches all fall outside standard general liability protection.

Filling Coverage Gaps With Add-Ons

Your business likely faces multiple liability exposures that a standard policy alone cannot address. Product liability, professional liability, cyber coverage, and commercial auto all protect against different risks. At Invest America Insurance, we work with multiple carriers to identify these gaps and fill them with targeted add-ons and bundled policies that protect your specific operation without paying for coverage you don’t need. Understanding what your general liability policy excludes helps you make informed decisions about which additional coverages your Nevada business actually requires.

Why Your Nevada Business Needs General Liability Coverage

Nevada’s Legal Landscape and Your Liability Exposure

Nevada law does not mandate general liability insurance for most small businesses, but this absence of requirement creates a dangerous misconception. Licensed contractors face strict requirements-electricians must carry $100,000 per occurrence and $300,000 aggregate minimums through the Nevada State Contractors Board, and these thresholds exist because the state understands that one uninsured claim can destroy a business. Your industry may not require the coverage by law, but your landlord almost certainly will. Commercial leases across Nevada consistently demand proof of general liability before you can occupy the space. Clients bidding work to your company will request certificates of insurance. The moment you sign a contract worth real money, you need this protection in place.

Nevada’s legal environment also matters-rate increases have been approved because litigation costs are rising. Lawsuits in Nevada are becoming more expensive to defend. If a customer suffers a serious injury on your property or your work damages their belongings, the legal bills alone can reach tens of thousands before settlement. Without coverage, that money comes directly from your operating account and personal assets.

The Real Cost of Going Uninsured

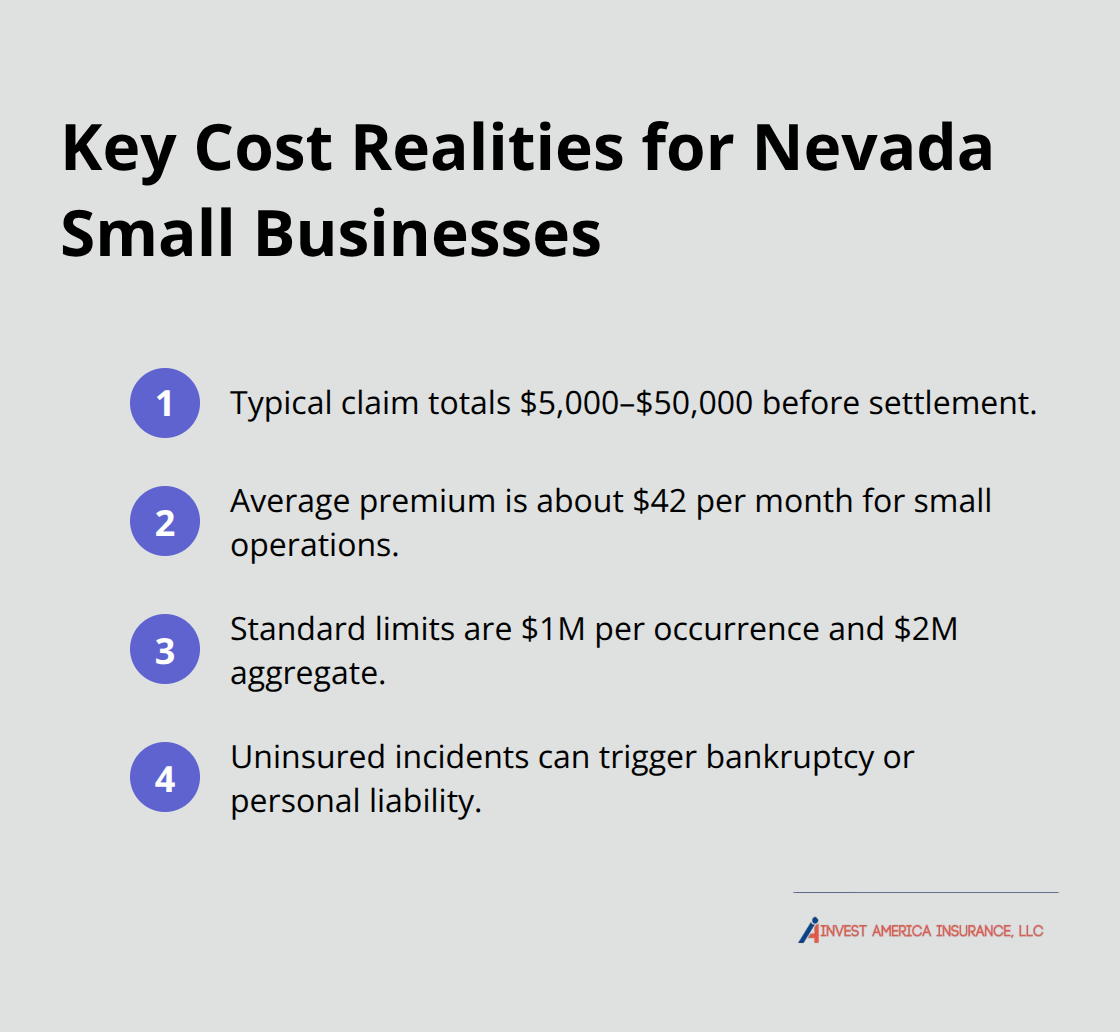

The financial reality of an uninsured claim is brutal. A customer slip-and-fall in a retail location, a contractor accidentally damaging a client’s home during a renovation, or an employee inadvertently causing property damage during service work-these incidents happen constantly across Nevada businesses. The average general liability claim costs $5,000 to $50,000 in medical bills, property repairs, and legal defense before any settlement or judgment.

Most Nevada small businesses choose $1 million per occurrence limits specifically because this amount covers typical incidents while staying affordable. General liability averages around $42 per month for small operations, according to industry data. That $504 annual investment protects your business from catastrophic loss. Without coverage, a single incident forces you to choose between bankruptcy and personal liability, meaning creditors can pursue your personal bank accounts and assets.

Finding Affordable Coverage That Fits Your Budget

The Hartford, Nevada’s top-rated option with a MoneyGeek score of 4.64 out of 5, and NEXT Insurance both offer flexible limits and digital policy management that let you access your certificate of insurance within minutes when a client or landlord demands proof. The cost of being uninsured far exceeds the premium you pay. As an independent agency, we at Invest America Insurance work with multiple carriers to find rates that fit your budget while maintaining adequate protection for your Nevada operation.

Your next step involves understanding exactly what coverage limits your specific business actually needs and how to compare policies across different carriers to secure the best protection at the right price.

How to Choose the Right General Liability Policy for Your Business

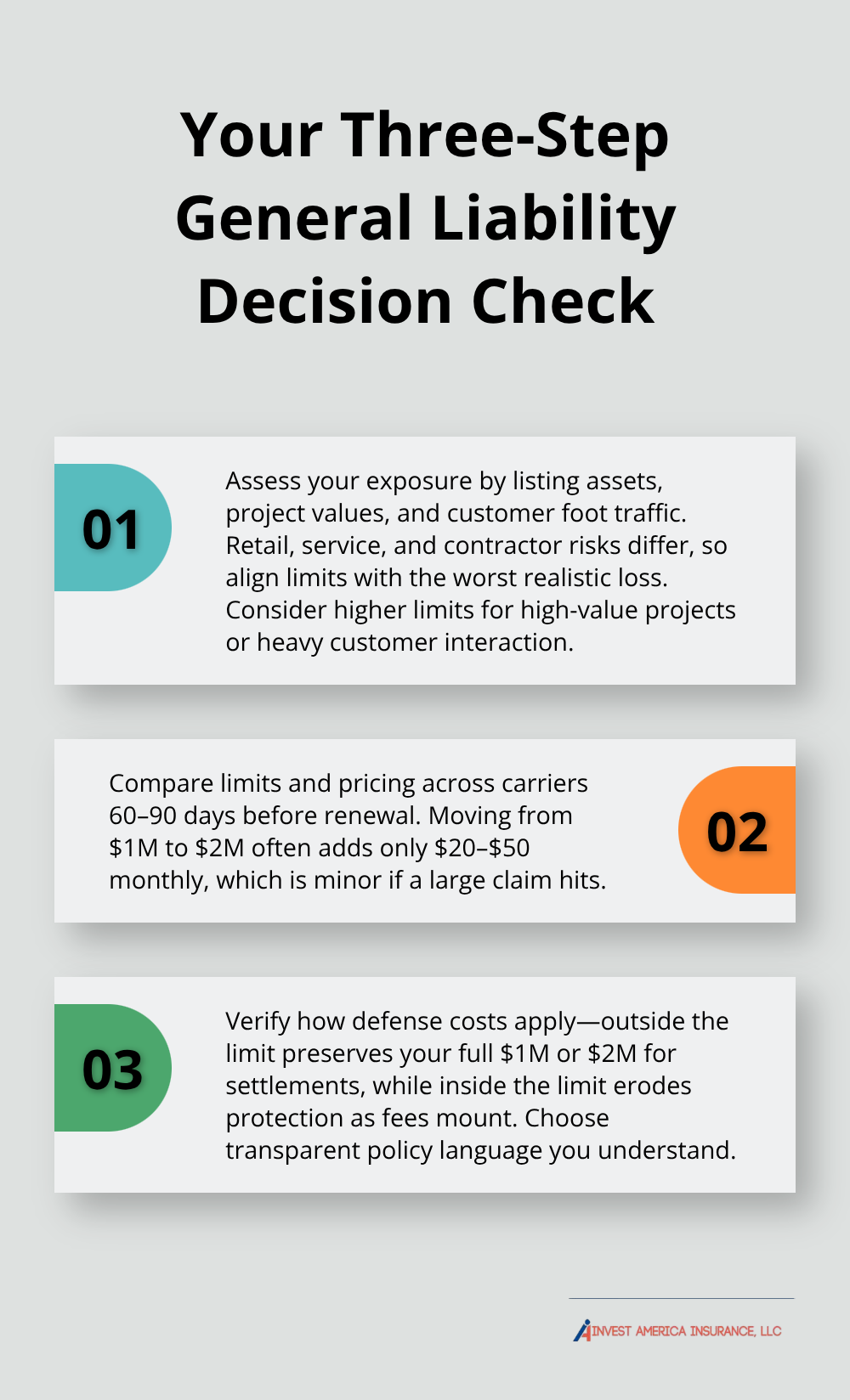

Assess Your Actual Business Exposure

Start by mapping what your business owns and what could realistically go wrong. A retail store faces different risks than a contractor or a service provider, and your coverage limits should reflect those specific exposures. A contractor working on high-value residential projects should consider higher limits because a single mistake during renovation can cause significant property damage. A retail operation with significant foot traffic might need higher limits if customers regularly interact with expensive merchandise or equipment. The Hartford and NEXT Insurance both offer flexible limits up to $2 million per occurrence, so you avoid one-size-fits-all pricing.

Ask yourself what the highest-value single job or project your business handles amounts to. How many customers or clients visit your property weekly? What’s the most expensive item a customer could damage? Your answers determine whether the standard $1 million limit works or whether you need more protection.

Compare Limits Across Multiple Carriers

Cost differences between limit tiers matter less than you think when you face real liability. Jumping from $1 million to $2 million per occurrence typically costs $20 to $50 more monthly, depending on your industry and location. That $240 to $600 annual difference becomes irrelevant if you face a $1.5 million claim and your policy maxes out at $1 million.

Request quotes from at least three carriers within 60 to 90 days before your renewal date, because carriers often offer better pricing during this window. The Hartford averages around $103 monthly in Nevada, NEXT runs about $100 monthly, and Nationwide comes in around $111 monthly according to MoneyGeek data. These premiums vary significantly by industry and location, so a pressure-washing business in Las Vegas might pay $200 to $300 monthly while a consulting firm in Henderson pays $40 to $60. Getting actual quotes for your specific business beats any general estimate.

Verify How Defense Costs Apply to Your Limit

When comparing policies, verify that defense costs count separately from your coverage limit rather than reducing it. This distinction affects how much protection you actually maintain after a claim. A policy that covers defense costs outside the limit preserves your full $1 million or $2 million for settlement or judgment. A policy that counts defense costs against your limit erodes your protection as legal bills accumulate.

Most Nevada small businesses select $1 million per occurrence and $2 million aggregate limits because these thresholds satisfy typical lease requirements and contract language while staying affordable. However, this standard approach fails many businesses. The Hartford and NEXT Insurance both offer transparent policy language that shows exactly how defense costs apply, so you understand your actual protection before you purchase.

Final Thoughts

General liability insurance in Nevada protects your operation from the financial devastation of third-party claims, and the coverage you select today determines whether a single accident becomes a manageable insurance claim or a business-ending catastrophe. Standard limits of $1 million per occurrence and $2 million aggregate work for most Nevada operations, but your specific industry, location, and contract requirements may demand different protection levels. Identify your actual liability exposure by examining what your business owns, how many customers interact with your property weekly, and what the highest-value project or transaction you handle amounts to.

Request quotes from multiple carriers within 60 to 90 days before your renewal date, because this timing window typically yields better pricing and allows you to compare how different insurers structure defense costs and policy limits. Verify exactly how defense costs apply to your policy limits and confirm that your chosen coverage aligns with lease requirements and client contract language, since these details often separate adequate protection from dangerous gaps. The Hartford, NEXT Insurance, and Nationwide all offer transparent policy structures that let you understand your actual protection before you purchase.

At Invest America Insurance, we work with multiple top-rated carriers rather than being tied to a single company, which means we shop around on your behalf to find general liability insurance in Nevada tailored to your specific situation. Most small operations pay less than $50 monthly for coverage that protects everything you’ve built. Contact us today to get quotes and secure the right protection for your business.