Turning 60 brings new financial priorities, and life insurance becomes more important than ever. At Invest America Insurance, we know that seniors over 60 face unique coverage challenges due to age and health changes.

Your family shouldn’t carry the burden of final expenses or outstanding debts. The right policy protects them while fitting your budget and health situation.

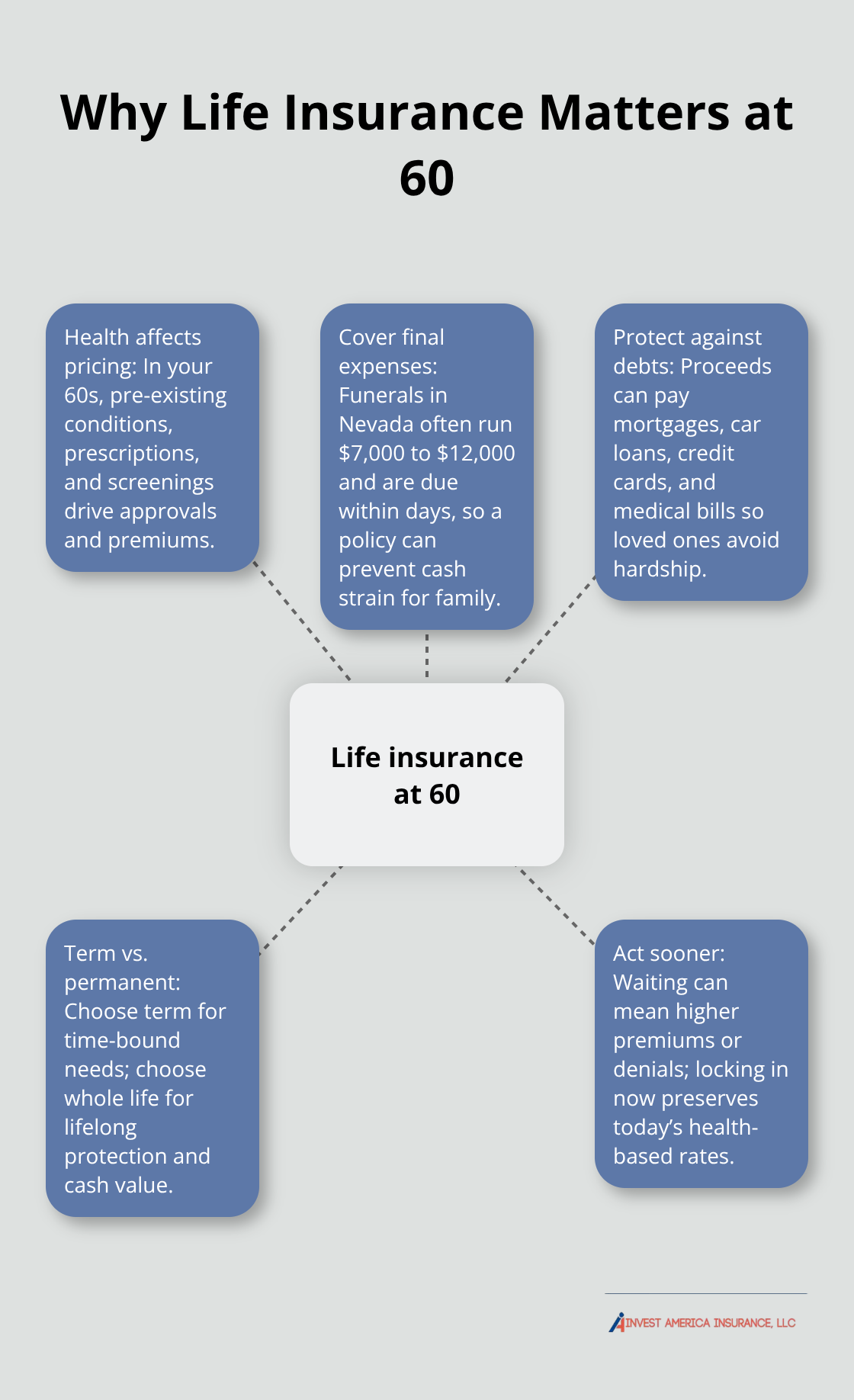

Why Life Insurance Matters for Seniors Over 60

Health changes shift your coverage options and costs

As you enter your 60s, your health profile shifts in ways that directly affect your insurance options and costs. Pre-existing conditions, prescription medications, and routine health screenings all factor into how insurers price coverage and whether they approve your application. The reality is stark: a 65-year-old nonsmoking woman pays roughly $215 per month for a $500,000 10-year term policy with Pacific Life, compared to significantly lower rates for someone in their 50s. Your health history matters more now, which is why acting sooner rather than later makes financial sense. Clients who delay coverage decisions often face steeper premiums or coverage denials later.

The window to lock in rates at your current health status closes quickly, and waiting five years can double or triple your monthly costs depending on age and any health changes that occur.

Final Expenses Create Immediate Financial Pressure

Average funeral costs in Nevada now exceed $7,000 to $12,000 when including burial or cremation, casket, and service expenses. Your family faces these bills within days of your death, and they must pay them regardless of their financial situation. Life insurance provides a lump sum that covers these immediate obligations without forcing your loved ones into financial hardship. A $250,000 policy for a 60-year-old costs roughly $131 per month for a 10-year term, yet it eliminates the burden of final expenses entirely.

Outstanding Debts Transfer to Your Family

If you carry debt-a mortgage, car loans, credit cards, or medical bills-your family faces the choice of liquidating assets or struggling with monthly obligations they may not afford. Life insurance prevents this scenario by providing funds to settle these obligations before they accumulate interest or damage your family’s credit. Whole life policies, though pricier at around $332 per month for $100,000 in coverage at age 60, offer lifetime protection plus cash value growth that your family can access if circumstances change.

Choosing Between Term and Permanent Coverage

The choice between term and permanent coverage depends on whether you need protection for a specific period (paying off a mortgage in 15 years) or indefinitely (leaving an inheritance or covering estate taxes). Nevada law gives you a 10-day free look period after your policy activates, so you can review the terms without penalty and cancel if it doesn’t fit your situation. Understanding these two main paths helps you move forward with confidence toward selecting the right policy type for your specific needs.

Which Type of Life Insurance Works Best for You

Term Life Insurance Covers Your Immediate Needs

Term life insurance covers you for a set period, typically 10 to 30 years, and costs far less than permanent options. For a 60-year-old in good health, a $500,000 10-year term runs about $253 per month, while a 20-year term costs roughly $485 monthly. This affordability makes term life the practical choice if you’re paying off a mortgage, covering a child’s education, or protecting income your family depends on during your working years.

The trade-off is straightforward: when the term ends, coverage stops. You won’t have a policy in place unless you renew or convert to permanent coverage before the term expires. Pacific Life and Protective both offer competitive rates for term coverage up to age 80 for shorter terms, though 30-year terms max out around age 50 to 58 depending on the carrier.

Nevada’s Grace Period Protects Your Coverage

Nevada’s grace period gives you a safety net if finances tighten. You can miss a payment and still maintain coverage while you catch up, preventing accidental lapses that would force you to reapply at higher rates.

Whole Life Insurance Provides Permanent Protection

Whole life insurance provides lifetime coverage with a cash value component that grows tax-deferred over time. At age 60, a $100,000 whole life policy costs about $332 per month, and by age 65 that same coverage rises to roughly $434 monthly. The higher premiums fund both your death benefit and the cash value account, which you can borrow against at low interest rates or withdraw from if you need funds during retirement.

This makes whole life valuable if you want permanent protection for estate taxes, a long-term dependent, or leaving an inheritance. The cash value grows steadily, giving you a financial asset that term life never provides.

Guaranteed Issue Life Insurance: When Health Limits Your Options

Guaranteed issue life insurance exists for those with serious health conditions that make traditional underwriting impossible, but it comes with a price: premiums run two to three times higher than underwritten policies, and death benefits cap much lower (usually between $5,000 and $25,000). The cost-to-benefit ratio is poor for most seniors, which is why guaranteed issue should only be your choice when traditional underwriting isn’t an option.

If you’re in reasonable health, an underwritten term or whole life policy delivers far better value. Penn Mutual offers no-exam coverage up to $10 million for applicants up to age 65, and Pacific Life allows no-medical-exam policies up to age 70, so even if a full medical exam concerns you, options exist that skip it without forcing you into guaranteed issue territory. Once you understand which policy type aligns with your financial goals and health situation, the next step involves comparing quotes across multiple carriers to lock in the best rates available to you today.

Sizing Your Coverage and Finding the Best Rates

Calculate Your True Coverage Needs

Determining how much coverage you actually need separates smart buyers from those who overpay or underpay for protection. Start by listing your financial obligations: remaining mortgage balance, car loans, credit card debt, medical bills, and final expenses. Add these figures together, then factor in any income replacement your family would need if you passed away. A 60-year-old with a $200,000 mortgage, $15,000 in car debt, $8,000 in credit cards, and $10,000 in final expenses needs at least $233,000 in coverage just to handle these obligations. Many seniors stop there, but that calculation misses whether your spouse or adult children depend on your income for household expenses. If your family relies on your income, multiply your annual earnings by the number of years until retirement or until your youngest dependent becomes self-sufficient. This gives you a realistic death-benefit target.

Avoid Overpaying for Unnecessary Coverage

Resist the temptation to buy more coverage than necessary just because rates seem low. Higher coverage means higher premiums forever, and that money could fund your retirement instead. For a 60-year-old in good health, a $250,000 10-year term costs roughly $131 monthly, while jumping to $500,000 pushes that to $239 monthly. That extra $108 per month compounds to $12,960 over ten years-money that disappears if you never collect the death benefit.

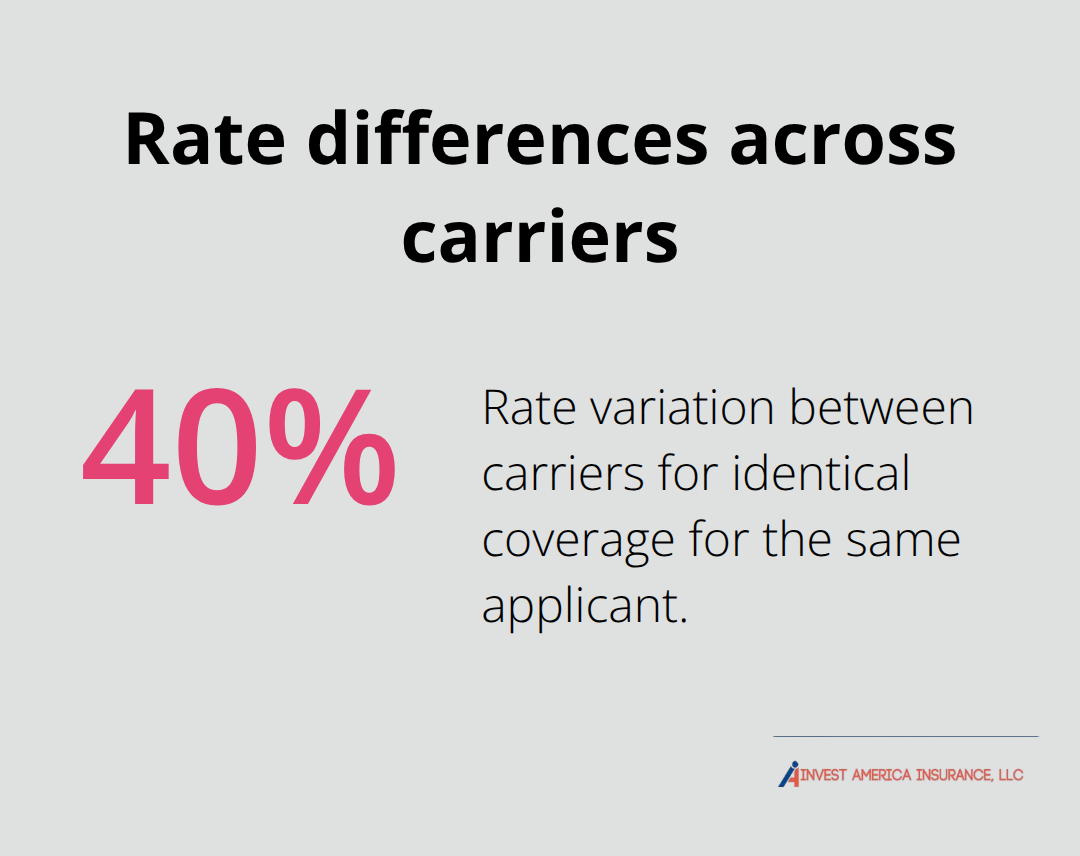

Compare Quotes Across Multiple Carriers

Comparing quotes across multiple carriers is non-negotiable if you want competitive pricing in Las Vegas. Pacific Life, Protective, Penn Mutual, and Nationwide all offer different rates for identical coverage, with variations sometimes exceeding 40 percent between carriers for the same applicant. Request quotes from at least three carriers before making a decision, and be honest on applications about health history, medications, and lifestyle habits-insurers verify this information, and misstatements can void your death benefit later.

Nevada’s contestable period lasts two years, meaning the insurer can challenge claims if they discover application errors during that window.

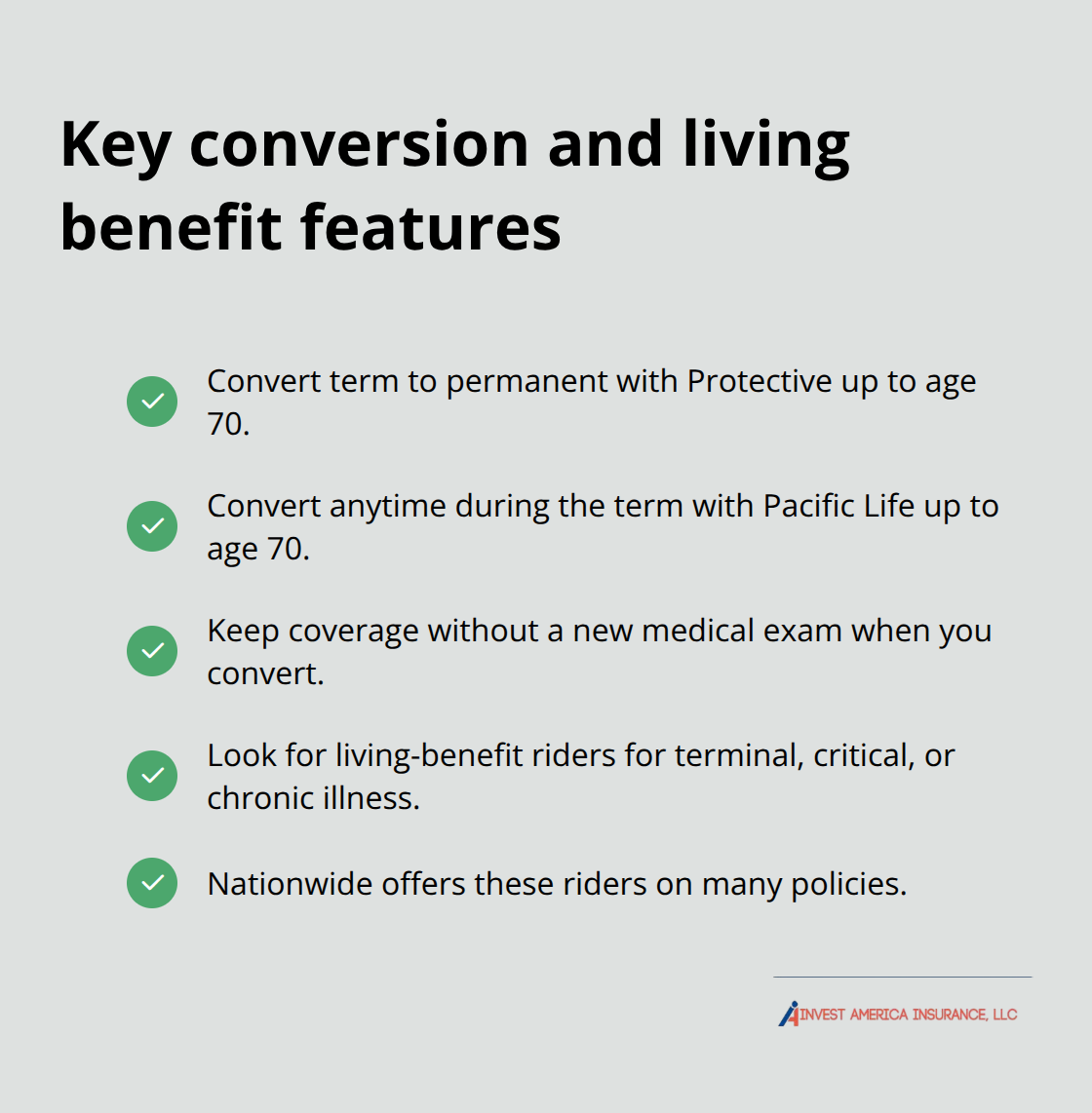

Understand Conversion Rights and Living Benefits

When reviewing policy documents, pay attention to conversion options if you buy term life. Protective allows conversion to permanent coverage up to age 70 but only within specific windows depending on your term length, while Pacific Life permits conversion anytime during your term up to age 70. These conversion rights matter because they let you lock in permanent coverage without another medical exam if your health deteriorates later. Confirm whether the policy includes living-benefit riders that let you access part of your death benefit early if you receive a diagnosis of terminal, critical, or chronic illness.

Nationwide offers these riders on many policies, giving you funds to cover medical costs or long-term care without waiting for death to trigger the benefit.

Get Expert Help Shopping Your Options

An independent agent can shop these options across multiple carriers on your behalf, ensuring you compare apples to apples and understand exactly what you’re buying before signing. This approach (working with an agent who represents multiple carriers rather than just one company) protects your interests and saves you time navigating the details of different policies and carriers.

Final Thoughts

Life insurance for seniors over 60 doesn’t have to be complicated, and you have clear options that fit different financial situations. A 60-year-old in good health can secure $250,000 in 10-year term coverage for roughly $131 monthly, while whole life at $100,000 runs about $332 monthly. Nevada’s 10-day free look period and grace period on missed payments protect you as you evaluate your decision and lock in the right policy.

Calculate your actual coverage needs by adding up debts, final expenses, and any income replacement your family requires, then request quotes from multiple carriers to compare rates. Don’t rush into guaranteed issue policies unless traditional underwriting truly isn’t an option, since underwritten policies deliver far better value. Pay close attention to conversion rights if you choose term life, and ask about living-benefit riders that let you access funds early for terminal or chronic illness (these riders can make a real difference in your financial flexibility during retirement).

Contact Invest America Insurance today to discuss your coverage needs and get personalized quotes that fit your situation. Our team works with multiple top-rated carriers to shop options on your behalf, ensuring you compare apples to apples and understand exactly what you’re buying. We act in your interest rather than pushing any single company’s products, and we help you lock in competitive rates before your next birthday.