Running an LLC in Nevada comes with real liability risks. One lawsuit or property damage claim could wipe out your personal savings if you’re not properly covered.

At Invest America Insurance, we help Nevada business owners understand exactly what business insurance for LLC operations should include. The right coverage protects both your company and your personal assets from unexpected financial disasters.

Why Your Nevada LLC Needs Business Insurance Now

Nevada’s business environment rewards growth, but it also exposes you to real financial liability. The state doesn’t require general liability or property insurance for LLCs-only workers’ compensation if you have employees-but that legal minimum leaves your personal wealth completely exposed. According to the U.S. Small Business Administration, Nevada has approximately 250,000 small businesses employing roughly 500,000 workers. Many of these business owners mistakenly believe that forming an LLC alone protects their personal assets. It doesn’t.

How LLC Formation Alone Fails to Protect You

An LLC provides liability protection only if you maintain proper insurance coverage and follow corporate formalities. Without business insurance, a single lawsuit, property damage claim, or injured customer can pierce that LLC protection and come directly after your personal bank accounts, home, and retirement savings. Nevada courts have upheld claims against LLC owners who failed to carry appropriate coverage, treating the business and owner as a single entity for liability purposes.

State Requirements Go Beyond the Basics

Nevada law mandates workers’ compensation insurance for any business with employees, but this covers only employee medical costs and lost wages-not your liability if a customer or third party gets injured on your property or because of your work. General liability insurance, while not legally required, is practically essential because commercial leases in Nevada almost always demand it, and most clients won’t work with uninsured contractors or service providers.

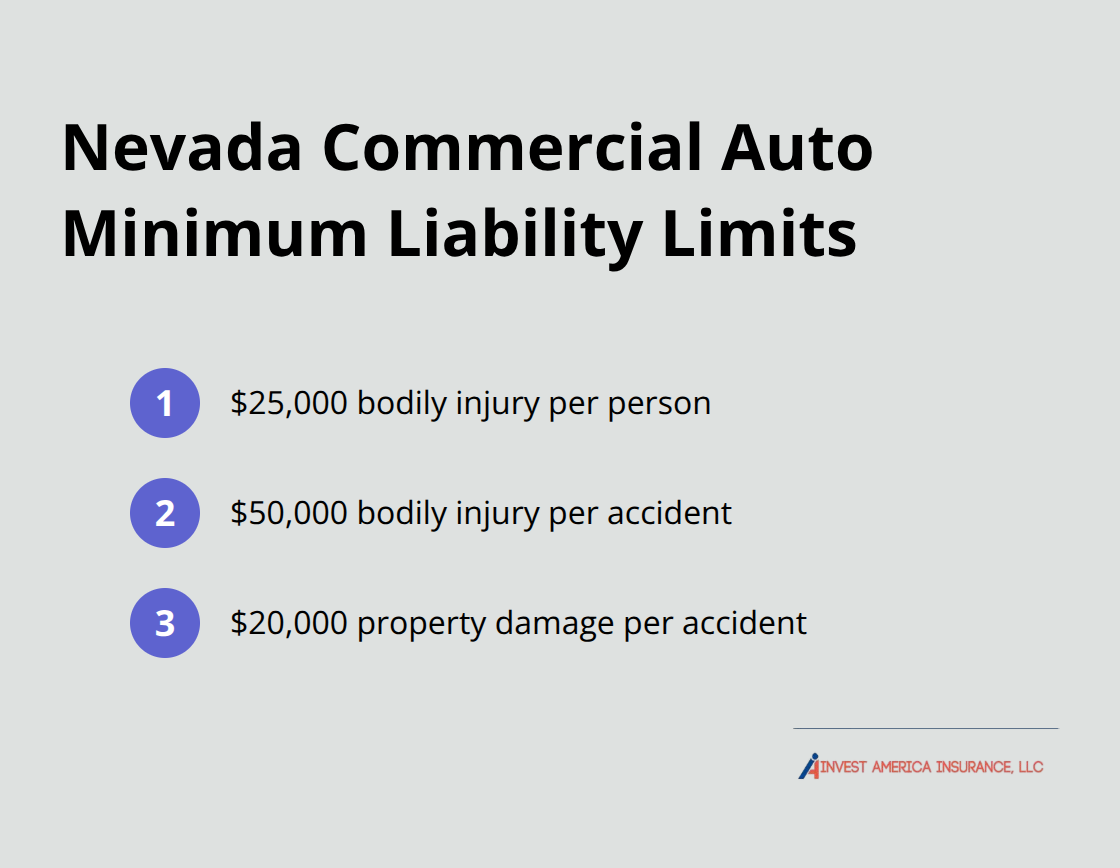

If you use vehicles for business, Nevada requires commercial auto insurance with minimum liability limits of $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage. Personal auto policies explicitly exclude business use, so driving a personal vehicle to client sites or job locations without commercial coverage leaves you personally liable for any accident.

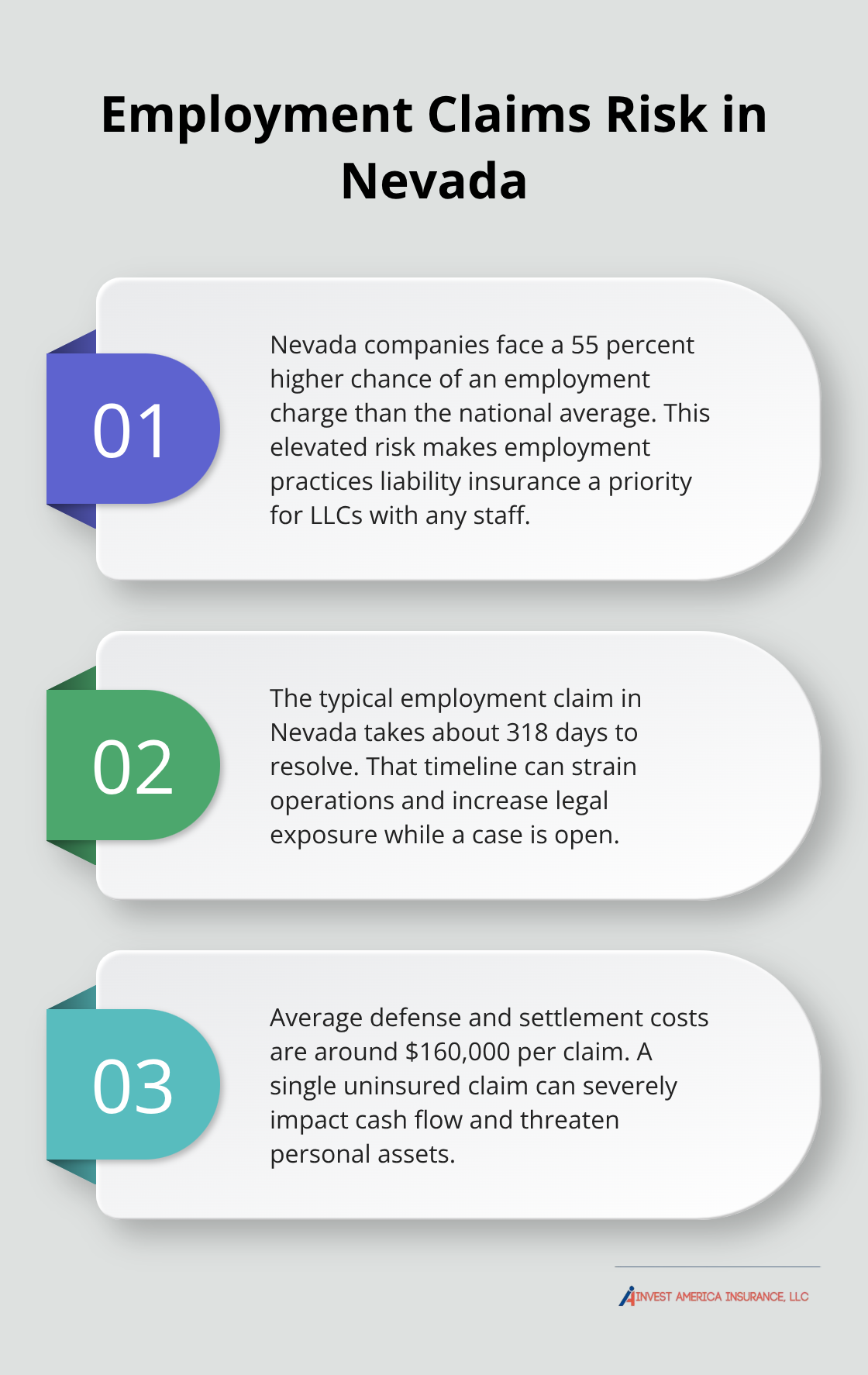

Employment discrimination claims carry particularly high costs in Nevada. Hiscox research shows Nevada companies face a 55 percent higher chance of an employment charge than the national average, with the typical claim taking 318 days to resolve and averaging around $160,000 in defense and settlement costs. That statistic alone should convince you that employment practices liability insurance belongs in your coverage plan.

Lenders and Clients Will Demand Proof

Banks and commercial lenders in Nevada won’t finance business operations without evidence of adequate insurance. If you’re seeking a business loan or line of credit, your lender will require a certificate of insurance naming them as an additional insured on your general liability policy. Major clients-especially in construction, real estate, hospitality, and professional services-won’t hire you without proof of coverage. They’ll ask for a certificate of insurance before you start work, and if you can’t provide one, you lose the contract.

Property owners and property managers require tenants to carry liability coverage, so if you lease commercial space, your lease agreement already mandates insurance. Skipping this step doesn’t just hurt your credibility-it can result in eviction or breach-of-contract liability. This requirement applies across Las Vegas and throughout Nevada, affecting nearly every LLC that operates from a commercial location.

Understanding what coverage types actually protect your business requires looking at each policy category separately. The next section breaks down the essential coverage types that Nevada LLCs need to consider.

The Three Coverage Types Every Nevada LLC Must Have

General Liability: Your First Line of Defense

General liability insurance protects your business against the most common claims you’ll face. It covers third-party bodily injury, property damage, and personal injury claims like defamation or false advertising. If a customer trips in your office and breaks their leg, or your work accidentally damages a client’s property, general liability covers medical bills, repair costs, and your legal defense.

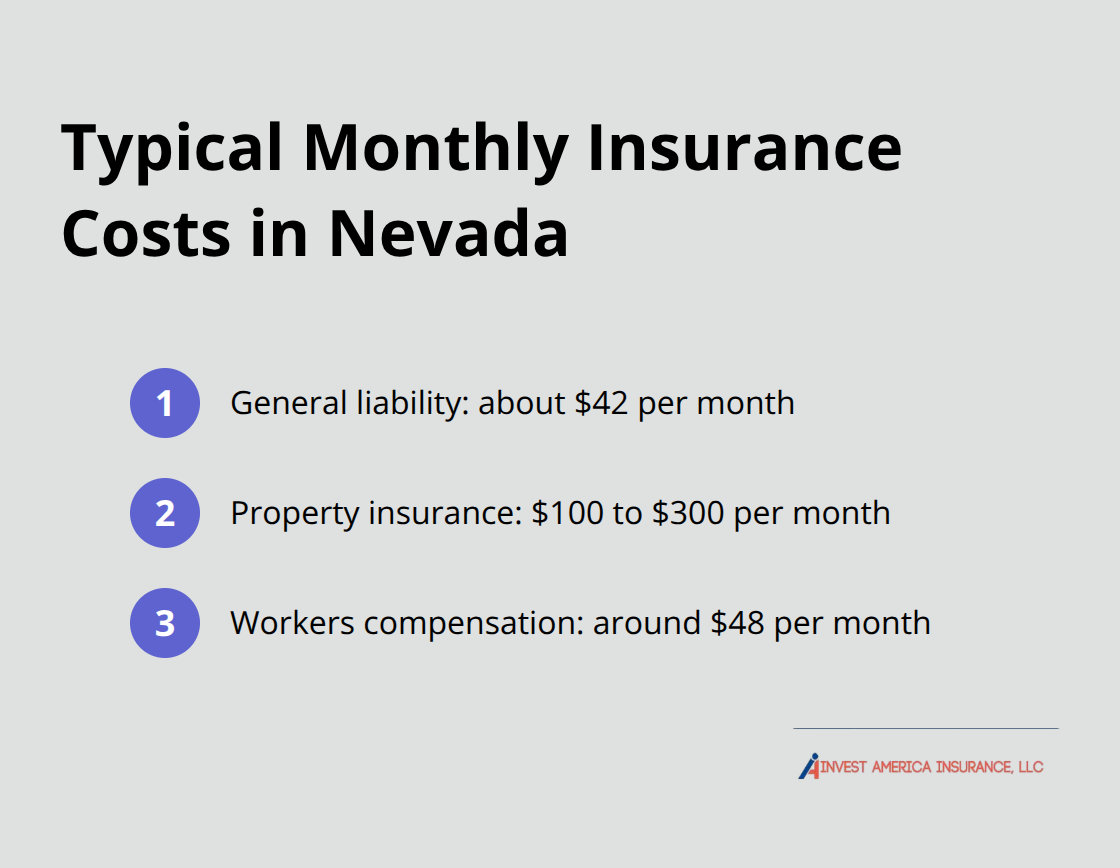

Nevada businesses typically pay about $42 monthly for general liability, though costs vary significantly based on your industry and operation size. A landscaper handling heavy equipment faces higher premiums than a consulting firm working from a home office. Nearly every commercial landlord in Nevada will refuse to lease space without proof of general liability coverage, making this policy non-negotiable if you operate from a commercial location.

Property Insurance: Protecting Your Physical Assets

Property insurance protects the physical assets your business depends on-equipment, inventory, furniture, and the building itself if you own it. This coverage reimburses you for losses from fire, theft, wind, or water damage, which are genuine concerns in Nevada’s desert climate where sudden storms and temperature extremes can destroy property quickly.

A typical small business spends $100 to $300 monthly depending on the value of assets being protected. Skipping this coverage means a single fire or break-in could force you to rebuild from nothing. Property insurance works best when bundled with general liability in a Business Owner’s Policy (BOP), which typically saves Nevada small businesses money compared to purchasing policies separately.

Workers Compensation: A Legal Mandate

Workers compensation becomes mandatory the moment you hire your first employee, regardless of whether they work full-time or part-time. Nevada law imposes steep penalties for non-compliance-fines up to $15,000, stop-work orders, and potential criminal charges if an employee is injured and costs aren’t covered.

The state calculates premiums based on your payroll and industry classification, with monthly costs averaging around $48 for small operations. High-risk trades like construction or tree removal see substantially higher rates. If you’re a sole proprietor without employees, you can typically exempt yourself, but the moment you bring someone onto payroll, this coverage becomes legally mandatory and non-negotiable.

Bundling Coverage for Maximum Protection

Combining these three coverage types into a single Business Owner’s Policy creates a more comprehensive safety net than purchasing them separately. Most Nevada LLCs benefit from this approach because it simplifies administration, reduces overall costs through bundling discounts, and eliminates coverage gaps that could expose your personal assets.

The specific mix of coverage you need depends on your industry, number of employees, and operational risks. Understanding your industry’s particular exposure-whether you handle client data, operate vehicles, employ staff, or work on client property-determines which additional coverages should complement your core three policies.

What Makes Nevada’s Business Environment Different for Insurance

Nevada’s insurance landscape demands different protections than other states, and LLCs operating here face specific environmental and regulatory exposures that directly impact coverage needs and costs.

Desert Climate and Property Risks

The desert climate brings genuine property risks that affect every Nevada business. Flash flooding in Las Vegas during monsoon season occurs particularly from July through September, with a 1999 monsoon storm that caused widespread flooding resulting in three inches of rain in some spots, two deaths, and more than $20 million in property damage.

Fire risk remains elevated year-round due to dry conditions and high winds. Spring months bring Santa Ana-style wind patterns that have sparked major brush fires near populated areas. Sudden temperature swings can damage equipment and inventory stored without climate control.

Property insurance premiums in Nevada reflect these environmental realities. Standard property policies exclude flood damage entirely-you need a separate flood policy to protect against this very real threat. Skipping property coverage means accepting the full financial burden of weather-related losses.

Nevada’s Regulatory Requirements

Nevada’s regulatory environment creates specific compliance obligations beyond workers compensation. The state requires commercial auto insurance with minimum liability limits of $25,000 per person and $50,000 per accident for bodily injury, plus $20,000 for property damage.

Certain industries face stricter requirements. Contractors must carry general liability and often need surety bonds. Licensed professionals in real estate, accounting, and engineering face specific E&O requirements that vary by licensing board. Las Vegas and Clark County add local ordinances that affect insurance requirements, particularly for businesses operating in certain zones or handling hazardous materials.

The Nevada Division of Insurance maintains updated licensing and coverage requirements that change periodically. Relying on outdated information costs money and creates compliance gaps.

High-Risk Industries in Nevada Markets

High-risk industries in Nevada markets face elevated liability exposure specific to their work. Landscaping and tree removal companies, construction firms, cannabis-related operations, restaurants and food service businesses, personal trainers, and cosmetologists all operate in environments with distinct risk profiles.

A tree removal company operating in the Las Vegas valley faces different risks than one in a different state due to dense residential development, mature trees in yards with pools and structures nearby, and the liability exposure that creates. Cosmetologists in Nevada deal with specific product liability and personal injury claims that differ from other service businesses.

Cannabis businesses, while not legally required to carry cannabis-specific insurance in Nevada, operate in a heavily regulated environment where local jurisdictions often impose additional insurance requirements as a condition of licensure or operation. Understanding your specific industry’s risk profile within Nevada’s market determines proper coverage. As an independent insurance agency based in Las Vegas, Invest America Insurance works with multiple top-rated carriers to shop around on your behalf and offer coverage options tailored to your business’s specific needs and risks.

Final Thoughts

Your Nevada LLC faces real financial exposure without proper business insurance. The three core policies-general liability, property insurance, and workers compensation-form the foundation that keeps your personal assets safe from business claims. Nevada’s specific environment, from desert weather risks to employment discrimination exposure, demands coverage tailored to your actual operations rather than generic policies designed for other states.

Start by reviewing your current coverage against the specific risks your business faces. If you operate vehicles for work, verify you have commercial auto insurance rather than relying on personal policies that exclude business use. If you have employees, confirm your workers compensation meets Nevada’s legal requirements and covers your actual payroll. If you lease commercial space, check that your property and liability coverage matches what your lease agreement demands.

Finding the right insurance partner matters more than finding the cheapest quote. You need someone who understands Nevada’s specific business environment and can match your coverage to your actual needs rather than selling you unnecessary policies or leaving gaps in protection. Invest America Insurance works with multiple top-rated carriers to shop around on your behalf and offer coverage options tailored to your business insurance for LLC Nevada operations.